China continued to dominate global manufacturing as well as the world market for solar photovoltaic; as a consequence, the country’s decision to constrain domestic demand led to turmoil in the industry as Chinese modules flooded the global market.

The

resulting oversupply of cells and modules drove down prices and helped

to open significant new markets, which counteracted the decline in

China’s installations. Meanwhile, cell and module production capacity

continued to increase.

Record-low auction prices, driven by lower

panel prices and intense competition, brought further consolidation in

the industry. Trade disputes also affected the industry, weakening

project pipelines in India and affecting growth in the United States.

Overall,

manufacturers had a challenging year with slim margins, and many

manufacturers sold panels at below the cost of production. Nonetheless,

competition and price pressures also led to investment in new,

more-efficient production capacity and to continued advances in solar PV

technology, particularly in China.

Module prices declined about 29%

in 2018, to a global average of 22.4 cents per watt, with the greatest

decrease occurring after China’s policy changes in May. By one estimate,

this helped lower the cost of installing 1 MW of solar PV by an average

of 12%.

As

of late 2018, the LCOE from plants in operation was at levels close to

or below the retail electricity price in some countries, and in some

cases even below wholesale electricity prices.

Record PPAs and tenders continued during 2018, with some announcements of prices in the range of USD 20 per MWh.

Very low bid pricesi were seen in several countries, including Brazil, India and Egypt (under USD 30 per MWh).

Saudi

Arabia announced the winning bid from its 2017 tender (USD 23.4 per

MWh), and a PPA was signed in Dubai at a new low for the United Arab

Emirates (USD 24 per MWh).

Germany held an auction for large-scale projects that attracted bids below EUR 40 (USD 45.8) per MWh for the first time, and solar PV beat wind energy in joint auctions, although average bid prices inched up during the year.

The

United States also saw long-term PPAs signed at record low prices for

solar generation (the lowest being under USD 24 per MWh) and for solar

PV-plus-storage (median bid price of USD 36 per MWh).

Some in the

industry consider tariffs in the USD 20 per MWh range to be a “new

normal” for winning tenders under ideal conditions (for example, high

solar irradiation, stable policy environment), although the average

solar PV LCOE remains somewhat higher.

There is a concern that

tenders have been favouring the most cost-competitive options and not

necessarily the most advanced or innovative technologies and designs.

Even so, tenders have driven a shift to market-oriented conditions in

many countries and to the introduction of new business models.

Trade

policies also influenced the industry in 2018, with two of the top three

country markets (India and the United States) placing new tariffs on

China, the world’s largest manufacturer and exporter of solar products.

Mid-year, the government of India placed a safeguard duty of 25% on solar products imported from China and Malaysia. Indian developers responded by stalling project construction or sourcing imports from other countries in the region, particularly Singapore, Thailand and Vietnam.

Along

with a general slowdown in Indian demand during 2018, the duty

contributed to a reported 37% reduction in solar cell and module imports

relative to 2017.168 By some accounts, however, it also led to

additions to domestic manufacturing capacity.

The United States

imposed tariffs on nearly all major sources of solar PV imports in early

2018. The prospect of tariffs led to domestic stockpiling in 2017 and

drove up panel prices in

the country, making domestic production more profitable and spurring some new manufacturing plant construction.

In

2018, however, the import tariffs reduced demand for US solar

installations, a trend that was partially offset by a flood of Chinese

panels entering the global market. Three additional sets of US tariffs

(on Chinese inverters and non-lithium batteries, on steel and on

aluminium) adopted during 2018 also affected the US solar industry.

Meanwhile,

in September the EU ended anti-dumping and antisubsidy measures that

had been in force since 2013 on cells and modules imported from China.

The European Commission determined that it was in the EU’s best interest

to allow the measures to lapse, given the region’s goal of increasing

the supply of renewable energy.

In turn, China ended anti-dumping and countervailing duties on solar-grade polysilicon from the EU.

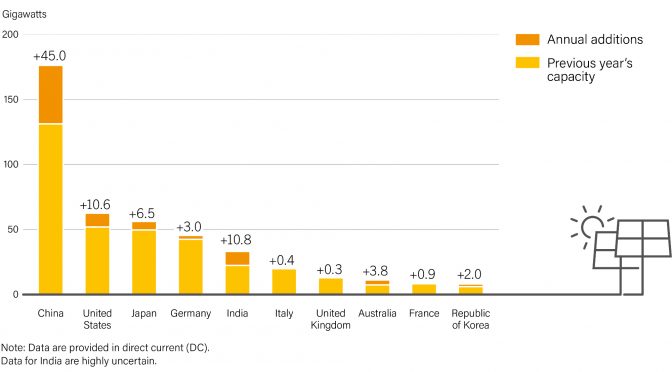

China

dominated global production in 2018 for the 10th year running. Seven of

the top 10 manufacturers, and all of the top three, were Chinese-based

companies: JinkoSolar maintained the lead, followed by JA Solar, Trina

Solar and LONGi Solar (all China); Canadian Solar (China/Canada), Hanwha

Q-CELLS (Republic of Korea), Risen Energy, GCL-SI and Talesun (all

China) and First Solar (United States) rounded out the top 10.

Most of these companies also were among the top 10 for cell production. First Solar is the only top 10 company that manufactures thin films and that produces all of its modules.

The

top 10 module suppliers shipped nearly 60% of the total in 2018.

Despite subsidy reductions and falling demand in China, several Chinese

companies made significant investments during 2018 to increase their

manufacturing capacity and announced plans for further expansion, with

the aim of achieving lower production costs through advanced

technologies.182 China’s cell production volumes were estimated to be up

more than 21% over 2017, to 87.2 GW, while module production rose

14.3%, to 85.7 GW.

Beyond China, new manufacturing capacity (mostly

for modules, and largely Chinese-owned) was completed or under

construction in several countries, including India, Morocco, Nigeria,

Saudi Arabia, South Africa, Sri Lanka and the United States (where

expansion has followed tax reform and trade tariffs).

Non-Chinese

manufacturers have found it increasingly difficult to compete due to

challenges they face in mobilising funding as well as to the growing

focus in China on high-tech manufacturing. As a result, many non-Chinese

manufacturers have turned to differentiation through products for niche

markets, specific technology add-ons and other developments that

provide added value.

While some companies in China have made

significant investments in manufacturing capacity and in research and

development in recent years, elsewhere around the world in 2018 most of

the capital flowing into solar PV went to downstream companies and

projects.

The year broke records for solar project acquisitions, with large projects attracting even conservative investors such as insurance companies and pension funds, and some 29 GW worth of solar projects traded hands.

Leading

utilities have acquired significant portfolios of solar PV projects; in

China, India and the United States, power companies have substantial

domestic capacity, whereas European multinationals are developing global

portfolios.

Companies upstream and downstream were affected by

cutthroat pricing that was not necessarily reflective of cost, as well

as by shrinking or shifting markets in some countries.

The year saw several bankruptcies, perhaps most notably in China, following the policy changes mid-year, and in Japan.

Since 2013, Japan has seen a steady rise in bankruptcies due to reductions in FIT payments and falling profits for solar companies: an estimated 95 Japanese solar companies went bankrupt in 2018.

In

India, very low energy prices from tenders made it difficult for

developers to get financing and to find equipment, particularly as the

industry remained highly dependent on imports. Even operations and

maintenance (O&M) companies felt the bite of price pressure, with a

notable increase in consolidation in India.

In response to such

pressures, O&M companies around the world continued investing in

labour-saving innovations and expanding into new service areas,

including energy storage.

The drive to increase efficiencies and

reduce the LCOE has pushed manufacturers to develop advanced

technologies, and new record cell and module efficiencies were achieved

throughout the year.

Silicon-based

solar cells, which account for about 90% of the market and are ahead of

the competition for stability and efficiency (20-22% for typical solar

cells in the marketplace), are close to reaching their maximum

theoretical efficiency. Researchers are working to overcome these limits

by stacking cells of different types and developing new cell

technologies.

Passivated Emitter Rear Cell (PERC) technology has

become the new standard for the monocrystalline silicon solar cell

variety because it increases efficiencies with modest investment.

PERC

cell production capacity increased from a few pilot lines in 2013 to

more than 35 GW in 2017, and was expected to exceed 60 GW by the end of

2018.

The large and rapid ramp-up has been driven in part by policy, with China leading the way.

Although

mono PERC is the focus of most capacity expansions, several

manufacturers are converting factories to production of heterojunction

cell technology (HJT), which offers higher efficiencies and can be

manufactured at relatively low temperatures and with fewer production

steps than other highefficiency cell technologies.

Researchers also

advanced perovskiteiv technology during the year, working to increase

efficiency and reduce costs, improve long-term stability and replace

lead content with more environmentally friendly materials. UK-based

Oxford PV announced a record 28% power conversion efficiency for a

perovskite-silicon tandem solar cell in late 2018, exceeding the

efficiency record for a single junction silicon solar cell (26.7%). The

company aims to make its technology commercially available by late 2019

or early 2020.

Module manufacturers have continued to develop advanced technologies, such as multi-busbars and half-cut cells, which were first used in China under the country’s Top Runner programme but increasingly are seen elsewhere as well.

By one estimate, at year’s end there were at least 15 technology options for modules, and the field was only expanding.

Bifacial modules, which can capture light on both sides, also offer significant potential gains in output that are expected to more than make up for their additional cost.

Large

projects with bifacial modules already were being deployed in 2018,

although quality-related uncertainties remained. First Solar took a

giant step forward with its transition to the Series 6 thin film module,

and in 2018 the company announced plans to triple its US manufacturing

capacity.

Improvements in geographic information systems are helping

developers identify locations with high solar resource potential for

large-scale projects, and other advances are helping to reduce time

requirements for project construction and commissioning.

More and more large projects are using single-axis trackers, which flatten the production curve and increase yield.

In 2018, global tracker shipments jumped an estimated 40%.

Once

projects are in operation, improved inverteriv reliability, remote

technologies and advanced cleaning options are helping to reduce

labour-related costs and outage times. Digitalisation is improving plant

monitoring processes, and new technologies such as aerial drones,

combined with artificial intelligence, are helping with preventative

maintenance, speeding up procedures, increasing plant efficiency and

reducing associated costs.

Despite tremendous steps forward in solar

PV technologies, the need to drive down manufacturing and project

development costs has raised concerns that manufacturers and developers

could be pushed to cut corners, and that quality could be compromised.

Already,

poor quality – from product manufacturing and shipping, to project

design and construction, to commissioning and O&M stages – is an

issue of concern in a number of countries.

In India, as a result of price pressure, inexperience, extreme climatic conditions and weak government requirements, many firms have cut corners on quality in order to operate on thin margins, so that they can bid low and win projects. Smaller rooftop systems in India have experienced quality challenges as well.

Other

countries, from Australia to Pakistan, also have faced component

quality issues due to the desire for cheap imported modules and to a

lack of testing and standards.

In turn, such developments have

prompted developers of large-scale projects to invest increasingly in

rigorous quality assurance programmes to secure return on their

investment in the medium and long term.

Governments and non-profit organisations, as in Australia, for example, have stepped up efforts to test and certify panels and other components in order to protect consumers.

As new technologies emerge, not only do they make decisions more complex for developers (for example, which module type to use, trackers or not), but there also is a need for new benchmarking tests.

Quality assurance companies, such as DNV GL of Norway, are working with universities and research institutions to advance and extend reliability and performance tests for modules.

In

2018, DNV GL issued the world’s first project certificate for a solar

PV plant to a 100 MW facility in Telangana, India. At the time, the

company’s service specification was believed to be the world’s only

global guideline for certifying solar PV projects.

To help reduce

uncertainty related to solar projects, large insurance companies have

begun guaranteeing output from solar farms. A new product sold by Swiss

Re AG, called a Solar Revenue Put, reportedly can guarantee as much as

95% of a solar plant’s expected output.

Other developments in 2018

included the opening in France of what was believed to be the first

non-pilot facility in Europe –and possibly the world – dedicated to

recycling solar panels.

In early 2019, Sembcorp and Singapore

Polytechnic signed a collaborative agreement to commercialise

Singapore’s first solar panel recycling process.

The linkages between

solar PV, storage and electric vehicles (EVs) continued to expand

during the year. Solar cell and module manufacturer Hanwha Q Cells

announced plans to enter the solar rooftop market with

solar-plus-storage for residential customers.

In

early 2019, the Dutch oil giant Shell purchased Sonnen, the leading

manufacturer of home batteries in Germany, with an eye towards becoming

the utility of the future – focused

on clean energy, EVs and distributed electricity generation with storage.

China’s BYD, which began by manufacturing batteries and later expanded into EVs, has begun manufacturing solar panels as well. In 2018, BYD and Kostal (Germany) signed a deal to provide storage solutions for residential and commercial solar PV systems.

In Germany, companies like Enerix, Sonnen and Solarwatt, which were once struggling due to a shrinking domestic solar PV market, are thriving thanks to the growing demand for energy storage systems.

https://ren21.filecloudonline.com/url/ysphuvhv4tyxcpm4

https://www.evwind.es/2019/06/21/wind-power-industry/67665