A stunning new report from French-based global banking group BNP Paribas signals the death toll for the petrol industry – a mixture of solar, wind power and electric vehicles can deliver more than six times the “mobility” returns on each dollar invested than oil.

The report, entitled “Wells, Wires and Wheels”, has been described as “seismic” by the likes of solar pioneer and entrepreneur Jeremy Leggett because he says it demonstrates the huge capital efficiency of wind turbines and solar and EVs over the petroleum industry. It suggests that the case for renewables and EVs over petroleum investments is “irresistible”.

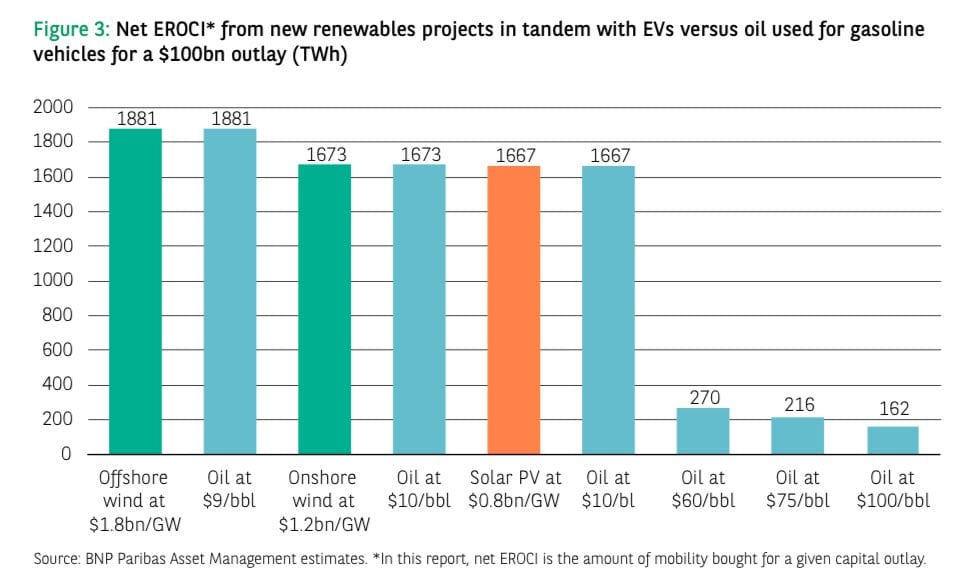

“We calculate that to get the same amount of mobility from gasoline as from new renewables in tandem with EVs over the next 25 years would cost 6.2x-7x more,” says the report, written by respected analyst Mark Lewis.

“Indeed, even if we add in the cost of building new network infrastructure to cope with all the new wind and/or solar capacity implied by replacing gasoline with renewables and EVs, the economics of renewables still crush those of oil.

“Extrapolating total expenditure on gasoline in 2018 for the next 25 years would see $US25 trillion spent on mobility, whereas we estimate the cost of new renewables projects complete with the enhanced network infrastructure required to match the 2018 level of mobility provided by gasoline every year for the next 25 years at only $US4.6 trillion to $US5.2trillion.”

Further, Lewis suggests that the only way that the petroleum industry could compete with renewables and EVs is if it could extract oil at around $US9-10 a barrel. The problem is, mid point return for most of the oil industry’s planned investments is a price of $US60 a barrel.

And his calculations are based on a rather conservative view of the costs of wind, solar and batteries – ranging from $US60/MWh to $US70/MWh for wind and solar, and modest capacity factors of 25 per cent for onshore wind and 15 per cent for solar. In Australia, those ratios should be doubled for new projects such as the Yandin wind farm (50 per cent) and most solar projects (more than 31 per cent).

Lewis suggests that the oil companies might be better off returning their money to shareholders, rather than continuing as usual.

Lewis also notes that these calculations are even before the climate- change and clean-air benefits, and the public-health benefits that flow from this are taken into account.

He says that while the oil industry has the advantage of incumbency, this may be time limited because of the rapidly changing nature of costs, and because it has never before faced the kind of threat that renewable electricity in tandem with EVs poses to its business model.

These, of course, are a competing energy source that (i) has a short-run marginal cost (SRMC) of zero, (ii) is much cleaner environmentally, (iii) is much easier to transport, and (iv) could readily replace up to 40% of global oil demand if it had the necessary scale.

“We conclude that the economics of oil for gasoline and diesel vehicles versus wind- and solar-powered EVs are now in relentless and irreversible decline, with far-reaching implications for both policymakers and the oil majors,” he notes in his summary.

“If all of this sounds far-fetched, then the speed with which the competitive landscape of the European utility industry has been reshaped over the last decade by the rollout of wind and solar power – and the billions of euros of fossil-fuel generation assets that this has stranded – should be a ashing red light on the oil industry’s dashboard.”

So, how does Lewis come up with these calculations?

This first graph (above) shows the gross potential of $US100 billion spent on gasoline. It can be expected to produce the equivalent of 2,824 terawatt hours of gross energy.

But from that you have to subtract the energy costs of refining, transportation and taxes, and then the refining losses, and finally the engine losses (most petrol cars run at a hopelessly low rate of efficiency of around 20 per cent, and Lewis says that is a generous estimate).

Compare that to solar, below.

For $US100 billion, you could expect to deliver gross energy of 3,249 terawatt hours, while the cost of transportation (per wires rather than pipes and ships) is much reduces, as are the energy losses in networks and the charging and battery losses.

In other words, the net return in “mobility” from the capital invested in petroleum is just 10 per cent of the energy produced. With solar and EVs it is 50 per cent.

That is no contest. And, as Lewis notes, this is without factoring in the huge cot savings from the ecological, social and security benefits of using renewables rather than oil.

Which makes Australia’s energy minister Angus Taylor’s plan to try and lock in a trans-Pacific delivery of emergency petrol supplies as daft as the government’s policy on renewables and electric vehicles – or the lack of them.

“With the economics of road transportation already moving so dramatically in favour of renewables in tandem with EVs, once the other advantages of renewables and EVs over oil as a road-transportation fuel are factored in the case for accelerating the roll-out of renewables capacity becomes unanswerable,” Lewis writes.

“We think that the implications of all this for both policy-makers and the oil majors are clear and compelling,” he says.

For policymakers, the economics of renewables are such now that there is a chance to accelerate the energy transition and the environmental and health bene ts that come with it by providing targeted support to:

– EVs, via tax incentives (as has proven very successful in Norway, for example)

– Charging infrastructure for EVs (the lack of charging infrastructure is a big obstacle to the faster adoption of EVs)

– Energy-storage technologies (as renewables increase their share of overall power generation, storage capacity will be the key to enabling continuing increases in renewables capacity)

Giles Parkinson is founder and editor of Renew Economy, and is also the founder of One Step Off The Grid and founder/editor of The Driven. Giles has been a journalist for 35 years and is a former business and deputy editor of the Australian Financial Review.