This update has been jointly prepared by the Global Wind Energy Council (GWEC) and the Chinese Wind Energy Association (CWEA) based on consultation with their industry members and their own market intelligence.

As China is the world leader in new onshore and offshore wind power installations, there have been rising concerns in over the impact of COVID-19 on the Chinese and global wind industry.

GWEC Market Intelligence interviewed six major Chinese wind turbine OEMs (which collectively held more than 75 per cent of Chinese market share in 2018), one foreign leading wind turbine OEM, one leading utility, one stock listed IPP, five leading component suppliers and one leading material supplier based in China. Following these discussions, we can conclude that the virus will impact supply chain and installation operations – however, the slowdown will not be as significant as reported by some industry observers (for example predicting a halving of China’s installations in 2020).

All respondents confirmed that operations have resumed following the extended Chinese New Year holiday, and that the local wind industry and government are both working to find solutions to minimise any adverse impact.

Delays expected in the manufacturing supply chain

In terms of wind turbine manufacturing, the major local Chinese turbine OEMs (Goldwind, Envision, Mingyang, Shanghai Electric, CSIC Haizhuang, DEC and CRRC) and three foreign turbine OEMs (Vestas, Siemens Gamesa and GE Renewable Energy) all resumed production in the week beginning 10 February. Other major component manufacturers – including NGC, Winergy, ZF (the world’s three leading wind gearbox producers), Yongji (China’s largest generator supplier) and Vertiv (a leading wind power converter exporter) – also confirmed that they resumed operations in the same week.

Although most facilities are not yet operating at 100 per cent capacity and many office-based employees are still working from home, the resumption of production means that the recovery to business-as-usual has already begun. It is also important to highlight that January and February are typically slower months for Chinese companies, due to the traditional Chinese New Year holidays, so observers should adopt caution in prematurely correlating a decline in production completely to COVID-19, although the virus will certainly be a factor in extending the slowdown.

Impact on installations in China will vary according to location

Developers evaluating the impact of COVID-19 on installations in the region believe that delays will be concentrated in Central and Southern China, rather than in North, Northeast or Northwest China. As China is a large country with varying weather conditions, it is typically too cold to begin foundation construction work in the latter regions in Q1 regardless.

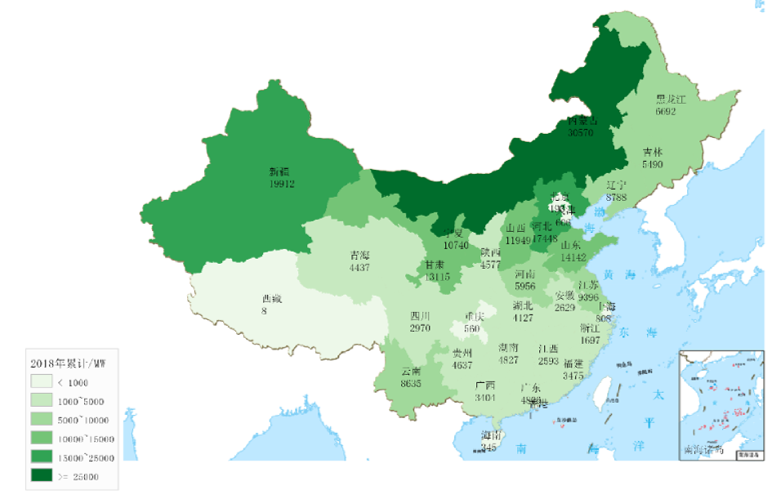

More than 40 per cent of new installations in China are located in North, Northeast and Northwest China, according to the Chinese Wind Energy Association (CWEA). With the ‘red alarm’, the risk warning mechanism adopted by China’s National Energy Administration (NEA) to control wind power installations in provinces with high curtailment rates, now being removed from provinces in northern China (including Xinjiang, Gansu, Jilin, Inner Mongolia, Ningxia and Heilongjiang), GWEC Market Intelligence expects more wind power to be added in these regions in 2020.

Considering South and Central China are significantly more populated, there are two main concerns: logistical delays, as many roads are still blocked due to the virus; and workforce capacity, due to lockdown of cities and 14-day quarantine requirements.

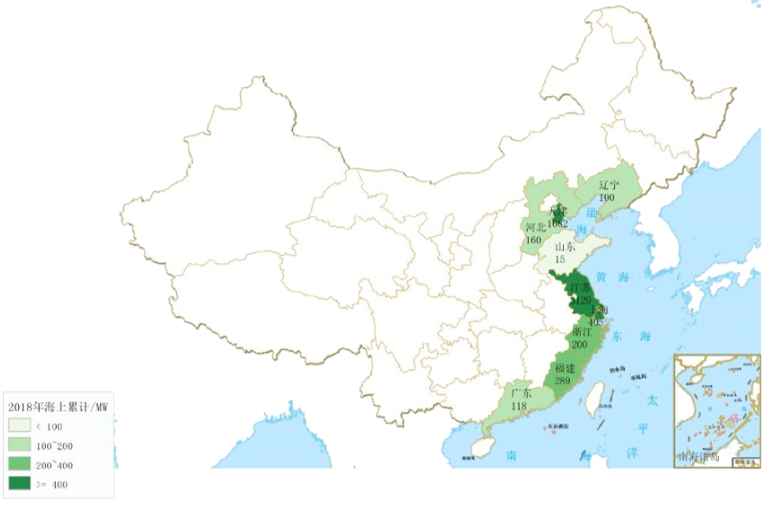

While workforce capacity remains a concern, these logistical bottlenecks are not as severe for the offshore wind industry. First, most offshore projects under construction are located in Guangdong, Jiangsu, Fujian and Zhejiang provinces, where there is less prevalence of the virus; and secondly, most offshore wind turbine and large component manufacturing facilities are near the coast and harbour, with shorter routes for deployment to offshore projects.

A possible FiT deadline extension keeps installation forecasts healthy

GWEC Market Intelligence has also been notified that the NEA has, in the week beginning 17 February, initiated an industry survey on the impact of COVID-19. The aim of this survey will be to assess the value of extending the onshore wind Feed-in-Tariff deadline set to expire on 31 December 2020. This extension, and other solutions, has been requested by the big five utilities in China, according to our conversations with industry.

If an extension is approved, it is expected that the number of onshore wind projects capable of capitalising on the Feed-in Tariff will not be revised, as the industry will rush to install projects within the extended deadline.

Impact on global supply chain is limited

GWEC Market Intelligence sees relatively less international impact of COVID-19, compared with the situation in China. The turbine assembly facilities of Vestas and SGRE in China are located in Tianjin, close to a major exporting port, and the World Health Organisation has not issued a warning on cargo transport vessels from China. It is also unlikely that countries will impose a unilateral import ban on Chinese goods as a precautionary measure for the virus, there OEMs will be able to continue exporting equipment.

For foreign turbine OEMs with facilities in China, their concerns centre on stabilising the flow of local components and increasing workforce capacity, which will certainly have impact on their production output in February and March. If these challenges cannot be resolved soon, foreign turbine OEMs that export to the US and Asia-Pacific markets from China are capable of mobilising their global footprint, employing untapped capacity in countries such as India to ensure they meet demand. This is the same strategy adopted by international gearbox suppliers under the current constraints of the U.S.-China trade conflict.

Ultimately, while COVID-19 will adversely impact the wind industry, the supply chain disruptions and installation delays will be moderate and focused to certain geographic regions. The Chinese wind industry has already begun picking up speed in the week beginning 17 February. If the virus out of Hubei province is more or less under control by mid-March, we can expect a roughly two to three month delay in executing China’s wind energy project pipeline. If the spread of the virus continues to grow beyond March, the delay period may be extended. However, these delays will be manageable if the NEA agrees to extend the FiT extensions of onshore wind.

Despite the material impacts and concerns of COVID-19, GWEC therefore assesses that China will continue to be the world’s largest wind power market in 2020, for both new onshore and offshore wind installations, with minimal impact on the global pipeline of wind projects. If the virus continues to grow beyond March, GWEC and CWEA will provide further updates on the impact for the wind industry.