Gas prices rose after several weeks of declines, dragging European Electricity markets.

In the second week of June, gas prices rose after keeping a downward trend since the second week of April. This, along with the increase in demand and in CO2 prices, led to the increase of prices in most of the European electricity markets. Even so, negative prices were registered in some markets during the weekend. In the French market, a daily record of solar photovoltaic energy production was reached on June 5.

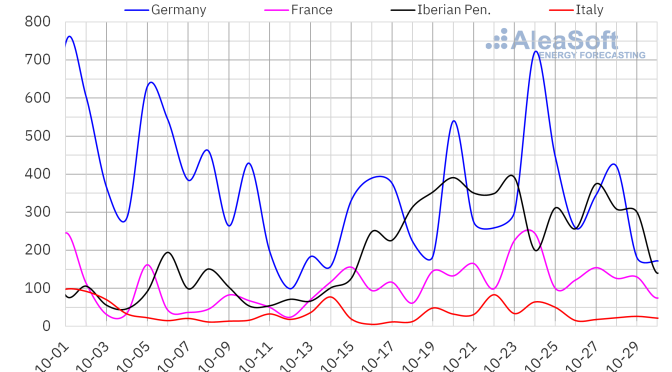

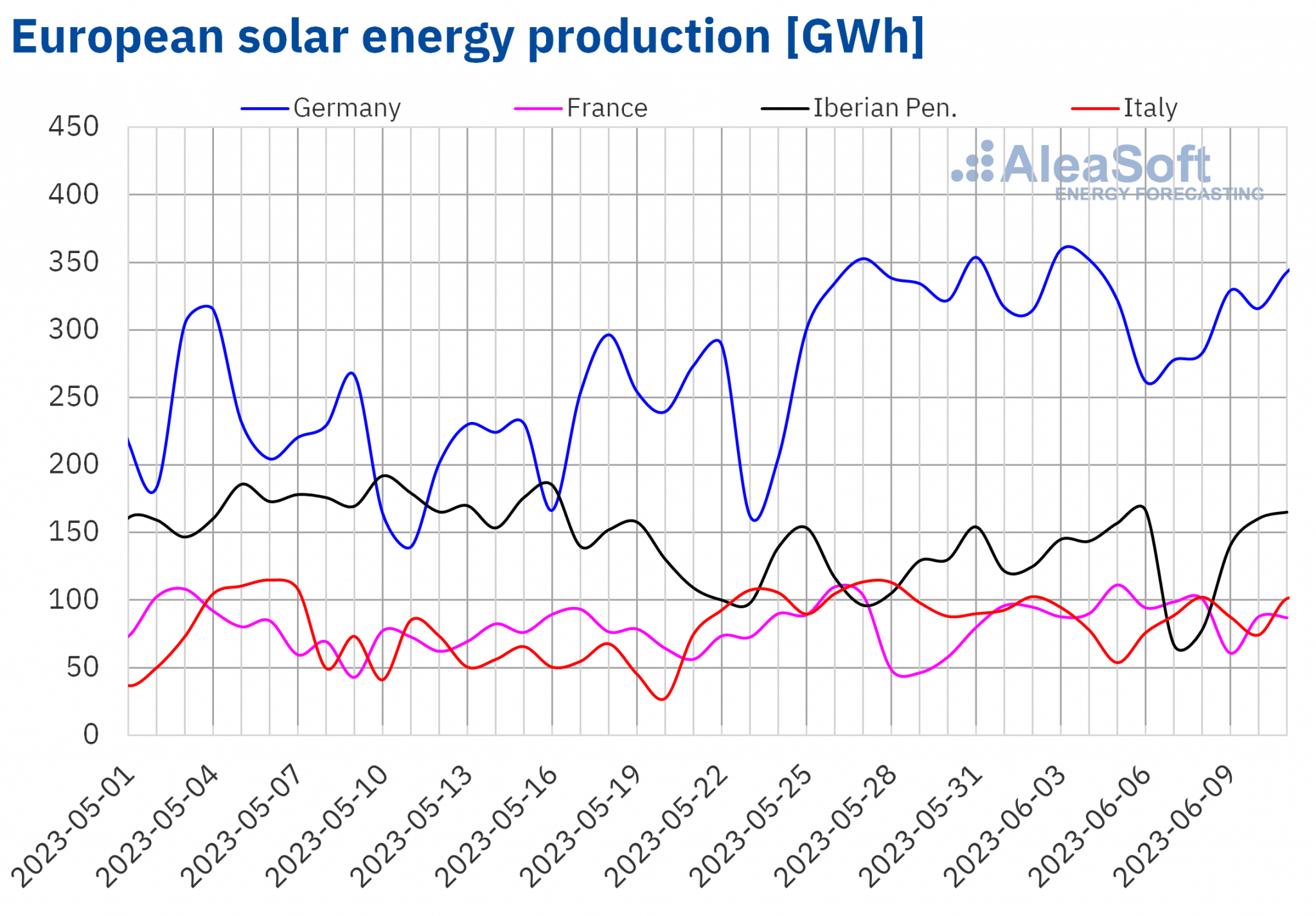

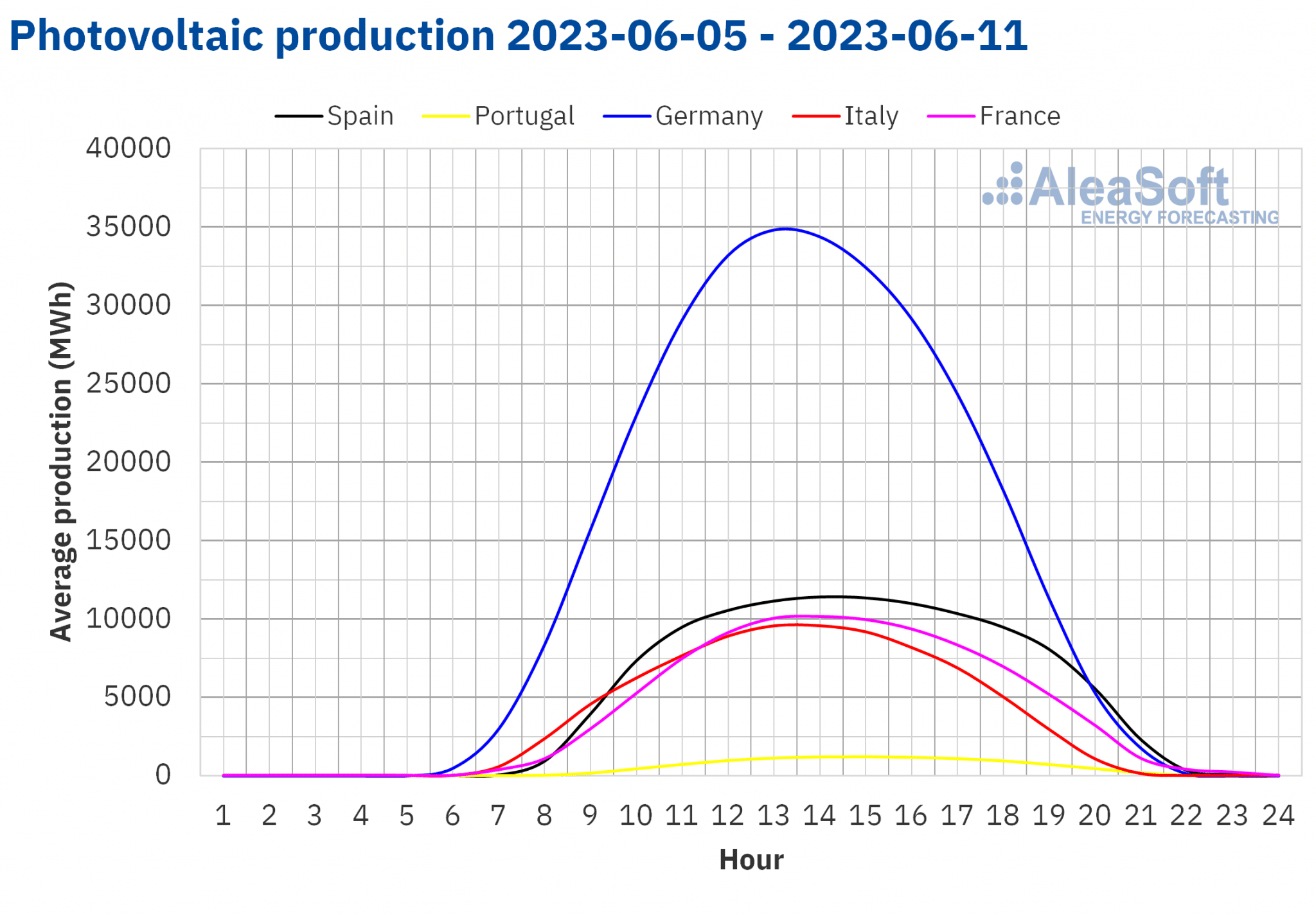

Solar photovoltaic and thermoelectric energy production and wind energy production

In the week of June 5, the solar photovoltaic energy production broke the daily record in the French market with 111 GWh generated on Monday, June 5.

Compared to the previous week, the French market was also the only one with an increase in the solar energy production among the main European markets analysed, with an increase of 16%. In the rest of the markets, a drop of 9.4% was observed in the German and Italian markets, as well as less pronounced decreases in the Iberian Peninsula of 1.3% and 0.1% in Portugal and Spain respectively.

For the week of June 12, the solar energy production forecasts of AleaSoft Energy Forecasting indicate that production will increase in Spain and Germany but could decrease in Italy.

Source: Prepared by AleaSoft Energy Forecasting using data from ENTSO-E, RTE, REN, REE and TERNA.

Source: Prepared by AleaSoft Energy Forecasting using data from ENTSO-E, RTE, REN, REE and TERNA.

In the week of June 5, the wind energy production increased in the markets of the Iberian Peninsula and Italy compared to the previous week, with rises of 184% , 102% and 23% in Portugal, Spain and Italy, respectively. On the other hand, drops were registered in the markets of France, of 44%, and Germany, of 11%.

For the week of June 12, the wind energy production forecasts of AleaSoft Energy Forecasting indicate that increases could be registered in Germany and Italy, while decreases are expected in the Iberian Peninsula and French markets.

Source: Prepared by AleaSoft Energy Forecasting using data from ENTSO-E, RTE, REN, REE and TERNA.

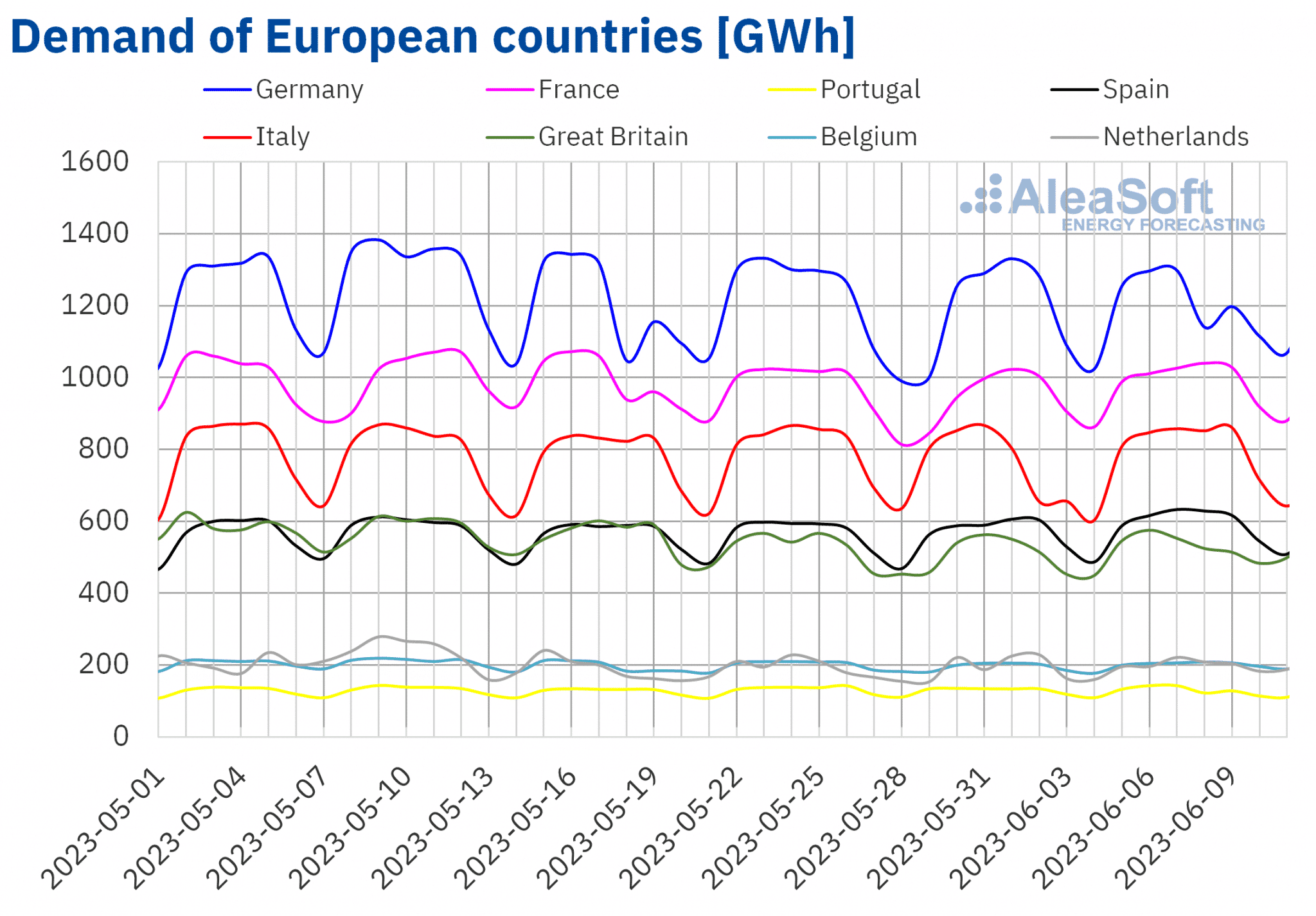

Electricity demand

The week of June 5 ended with an increase in electricity demand in almost all analysed European markets compared to the previous week, except in the Portuguese market where a decrease of 0.6% was registered, favoured by the Corpus Christi holiday celebrated on June 8. The largest rise, of 6.6%, was registered in the Italian market, followed by increases of 4.8% and 4.7% in the markets of Great Britain and France, and 4.4% and 4.3% of the Dutch and Spanish markets, respectively. On the other hand, the German market, where the Corpus Christi holiday was celebrated in some regions, registered the smallest increase of 1.2%.

In the case of the markets of Germany, Belgium, France, Great Britain and the Netherlands, the increase in demand reflects the recovery of the holiday of May 29, Whit Monday. In the case of the Italian market demand recovered after the Italian Republic Day, celebrated on June 2.

At the same time, average temperatures increased compared to the previous week in all markets analysed, with increases ranging from 0.9 °C in Italy to 4.4 °C in the Netherlands.

For the week of June 12, according to the demand forecasts of AleaSoft Energy Forecasting, a rise in demand is expected in all the main European markets analysed except in the Belgium market.

Source: Prepared by AleaSoft Energy Forecasting using data from ENTSO-E, RTE, REN, REE, TERNA, National Grid and ELIA.

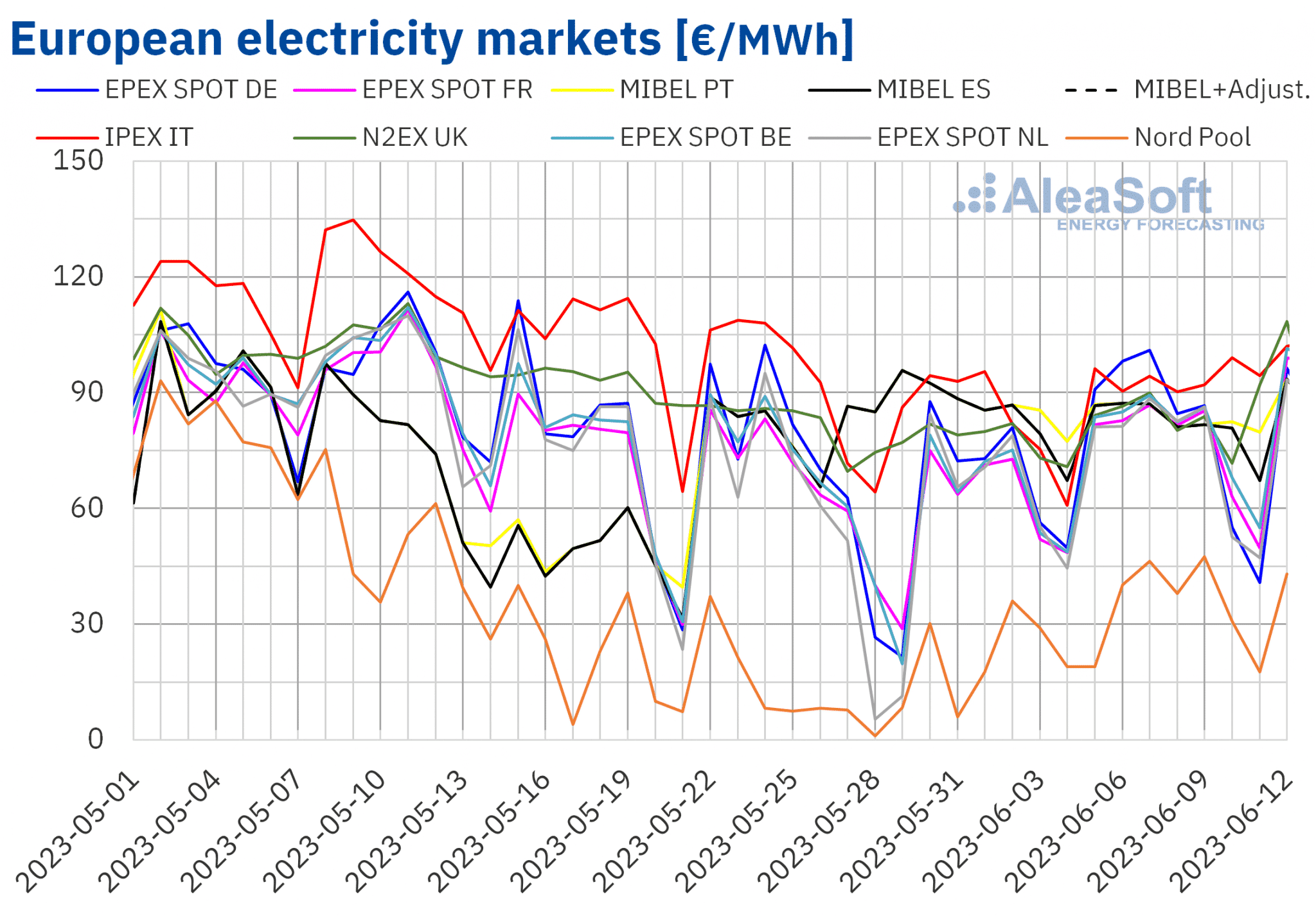

European electricity markets

In the week of June 5, prices of most European electricity markets analysed at AleaSoft Energy Forecasting increased compared to the previous week. The exception was the MIBEL market of Spain and Portugal, with decreases of 4.0%, and 4.1%, respectively. On the other hand, the most significant rise in prices, of 64%, was registered in the Nord Pool market of the Nordic countries. In the rest of the markets, prices increased between 8.2% of the N2EX market of United Kingdom and 33% of the EPEX SPOT market of Belgium.

In the second week of June, European markets’ weekly average prices remained below €95/MWh. The highest average price, €93.76/MWh, was that of the IPEX market of Italy. On the other hand, the lowest weekly average was that of the Nordic market, of €34.19/MWh. In the rest of the analysed markets, prices were between €74.21/MWh of the Dutch market and €84.01/MWh of the British market.

Regarding hourly prices, negative values were registered in the German and Dutch markets on June 10 and June 11. The Belgian, French and Nordic markets also registered negative hourly prices on Sunday, June 11. The lowest hourly price of the second week of June, of -€66.67/MWh, was registered on Sunday, June 11, from 13:00 to 14:00, in the Dutch market.

During the week of June 5, the increase in the average price of gas and CO2 emission rights, as well as the increase in demand in almost all markets, led to price increases in the European electricity markets. In the case of the German and French markets, the decline in wind energy production also contributed to this behaviour. In the Iberian market, on the other hand, there was a significant increase in wind energy production, which allowed prices to fall slightly.

Price forecasts of AleaSoft Energy Forecasting indicate that in the third week of June prices may keep increasing in most European electricity markets, influenced by the increase in demand.

Source: Prepared by AleaSoft Energy Forecasting using data from OMIE, EPEX SPOT, Nord Pool and GME.

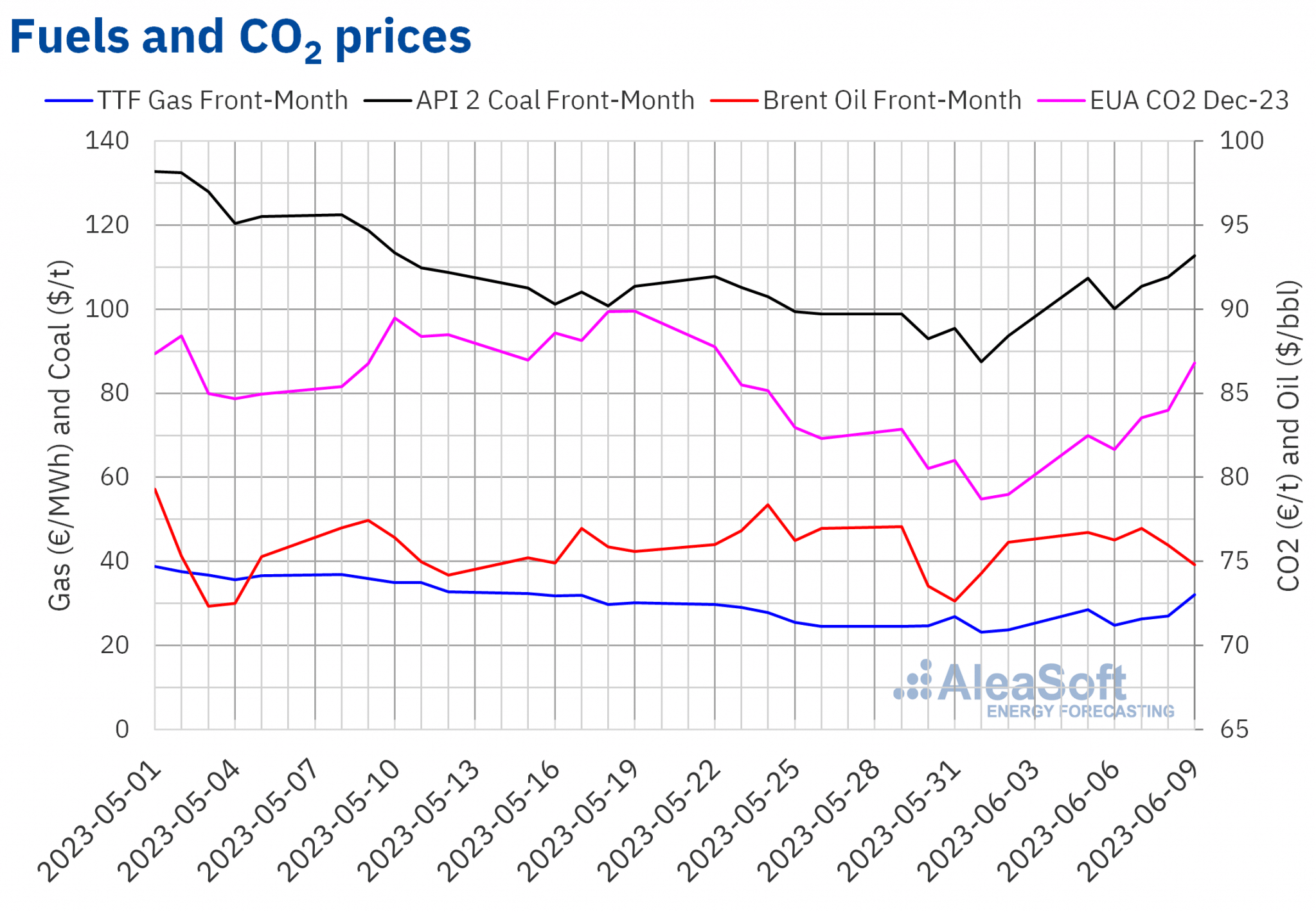

Brent, fuels and CO2

During the first days of the second week of June, settlement prices of Brent oil futures for the Front?Month in the ICE market were above $76/bbl. On Wednesday, June 7, the weekly maximum settlement price, of $76.95/bbl, was reached, which was 5.9% higher than that of the previous Wednesday. However, later prices decreased till reaching a weekly minimum settlement price of $74.79/bbl, on Friday, June 9. This price was 1.8% lower than that of the previous Friday.

On Sunday, June 4, the OPEC+ decided to maintain its production cuts until the end of 2024. Saudi Arabia also committed to additional cuts from July onwards. This exerted its upward influence on prices in the second week of June. But data on the Chinese economy and concerns about demand developments pushed prices lower in the last sessions of the week.

Regarding the TTF gas futures in the ICE market for the Front?Month, on Monday, June 5, a settlement price of €28.48/MWh was reached, 16% higher than that of the previous Monday. However, on Tuesday, June 6, a drop of 13% respect the previous day was registered and the weekly minimum settlement price, of €24.86/MWh, was reached, although this price was still 0.7% higher than that of the previous Tuesday. Later, prices rose and on Friday, June 9, the weekly maximum settlement price, of €32.05/MWh, was reached. This price was 35% higher than that of the previous Friday and represented an increase of 19% respect to the settlement price of Thursday, June 8. As a result of these increases, the weekly average rose by 13% from the previous week. Since the week of 10 April, the weekly averages had been falling continuously.

In the second week of June, problems in supply from Norway continued to influence TTF gas futures prices upwards. In addition, competition from Asian markets for liquefied natural gas supplies from the United States also contributed to the price increases.

Regarding settlement prices of CO2 emission rights futures in the EEX market for the reference contract of December 2023, during the second week of June, increases were registered on almost every day. The exception was that of Tuesday, June 6, when after a decrease of 1.0% compared to Monday, a weekly minimum settlement price of €81.66/t was reached. This price still was 1.4% higher than that of the previous Tuesday. On the other hand, as a result of the increase in prices, on Friday, June 9, the weekly maximum settlement price, of €86.79/t, was reached, which was 9.9% higher than that of the previous Friday.

Source: Prepared by AleaSoft Energy Forecasting using data from ICE and EEX.

AleaSoft Energy Forecasting’s analysis on the prospects for energy markets in Europe and the financing and valuation of renewable energy projects

On Thursday, June 8, the webinar number 34 of AleaSoft Energy Forecasting and AleaGreen was held, with the participation of speakers from Engie. The discussed topics in this webinar were the financing of renewable energy projects, PPA, the energy markets prospects in the second half of 2023 and the main regulatory issues of the electricity sector.

The next webinar of the monthly webinar series of AleaSoft Energy Forecasting and AleaGreen is scheduled for July 13. In this case, beside the evolution of energy markets and financing of renewable energy projects, the use of probabilistic metrics for the derivation of long-term electricity market price forecasts will be analysed. This webinar will also be on the main vectors of the energy transition. On the other hand, Roger Font, Director Project Finance Energy at Banco Sabadell y Josep Montañes, Corporate General Manager at Ecoener, will participate in the analysis table of the webinar in Spanish.