The scale of the opportunity for low-carbon technologies is mind-boggling. Eliminating emissions from a global energy system that today is 80% dependent on fossil fuels will require multiple low-carbon sources of energy to be developed, and fast. The US$70 trillion of investment that we estimate is up for grabs over the next three decades to reach the goals of the Paris Agreement will be at the centre of debate at COP28 in December.

Capital will flow into new technologies only if the policy support, including incentives, is right. The EU’s REPower EU and the US Inflation Reduction Act set a positive tone. But fostering emerging technologies is fraught with risks – for every one that breaks through, plenty will fail. Policymakers in all jurisdictions will have to scrutinise progress and adapt incentives to ensure the money piles behind the blossoming successes and lets failures wither away. Collaboration between countries and companies will be essential to mitigate early-stage risks and accelerate deployment at scale.

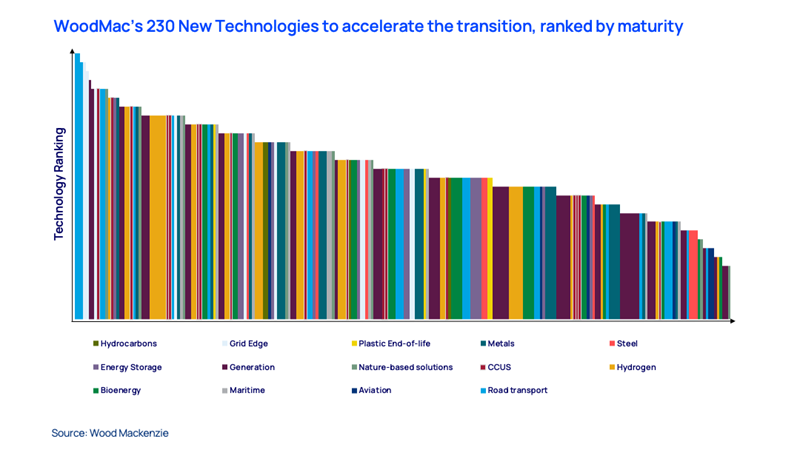

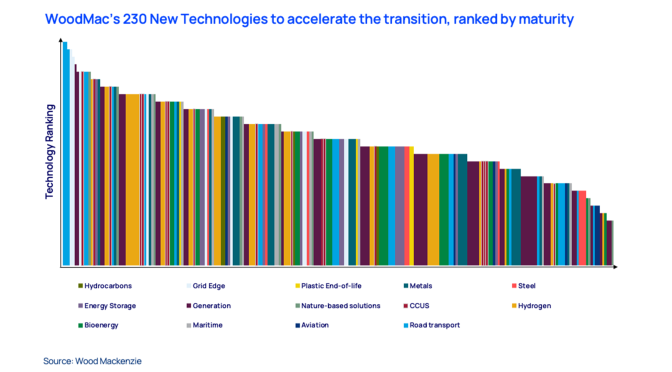

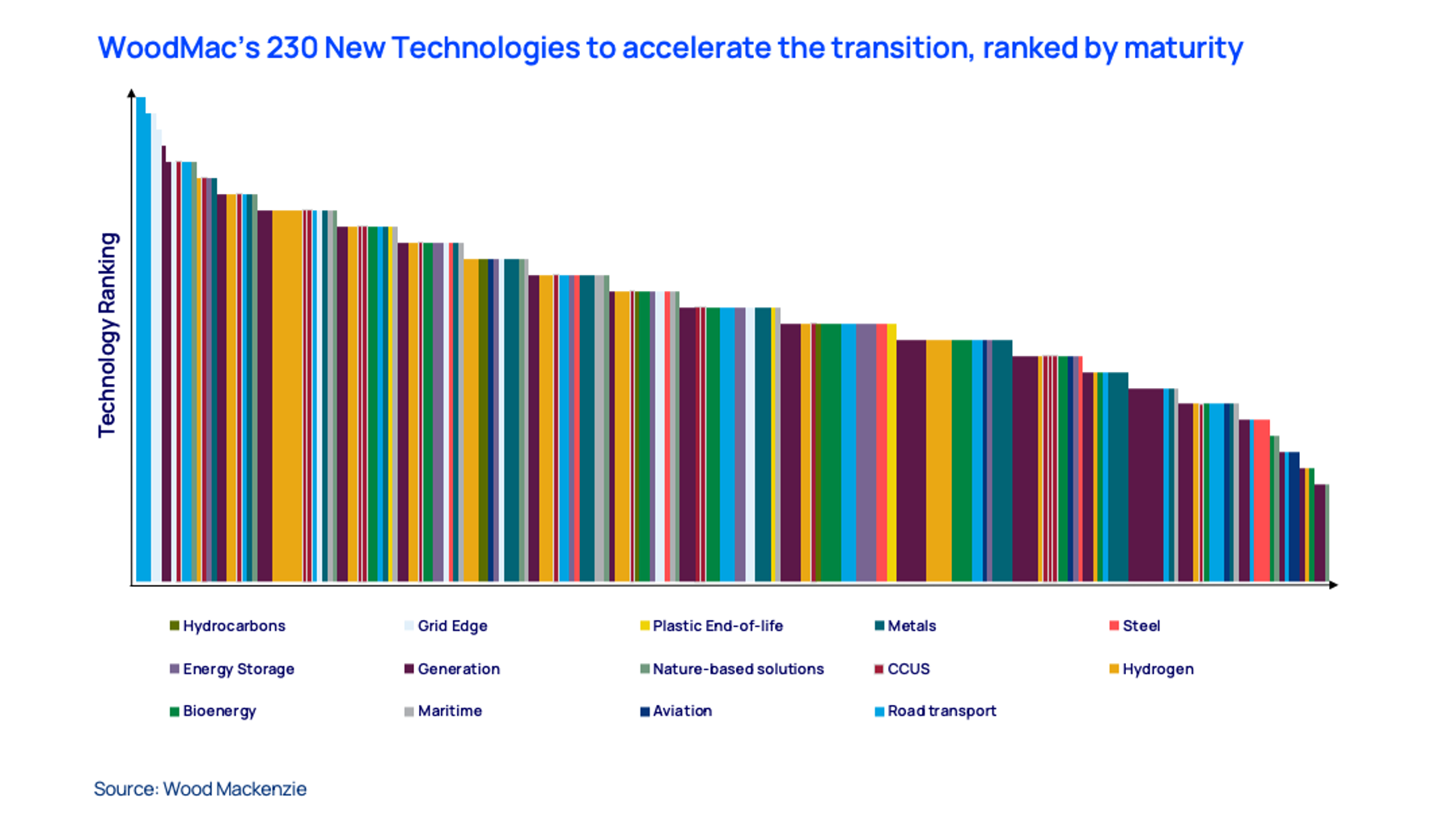

The pool from which winners will emerge is deep. The third edition of Wood Mackenzie’s New Technologies Series ranks 230 different technologies, each at various stages of development. Mature, ready-for-market technologies that are already attracting investment sit at the top of the rankings, among them renewables, electric vehicles and other technologies underpinning the electrification of transport.

But what’s the next wave to break through? Wood Mackenzie’s energy transition research team – Prakash Sharma, Jom Madan and Lindsey Entwistle – picked out five technologies moving up the rankings that we believe will make a meaningful impact on the transition.

Carbon capture utilisation and storage

The project pipeline has built up rapidly to 480 Mt but still needs to grow ten-fold to reduce global emissions by 15% to 20% and meet net-zero targets by 2050. We estimate a US$150 billion investment opportunity over the next 10 years.

A huge ramp-up in CO2 storage licensing over the past year and an active M&A market with Big Oil and NOCs doing large-scale deals and partnering are strong indicators that CCUS is the fastest maturing of the five.

Project announcements have slowed as developers look to execute. The technology is well understood but not fully proven commercially with questions around reliability, performance and scalability. Plus, it’s expensive (US$20 to US$400/t CO2, depending on CO2 source). Parts of the value chain have been overlooked, among them emitter uptake (which lags storage capacity) and transportation from source to storage. Policy support is needed to create the industry, with the US and Canada ahead of Europe and Asia on targeted incentives.

Much of the present focus for CCUS is on decarbonising natural gas production. The real impact though will be made in hard-to-electrify sectors such as steel, cement and chemicals. Large-scale CO2 shipping is also required to help countries lacking sequestration capacity domestically – especially relevant for potential sinks in Northwest Europe and Asia Pacific.

Hydrogen

The hottest emerging low-carbon fuel. Hydrogen’s potential to play a critical role in the transition can’t be understated: it’s capable of delivering 20% of the emissions reductions needed for net zero by 2050 from a standing start. But it will be a decade before capacity reaches material scale.

The project pipeline tallies over 90 Mtpa currently and needs to grow six-fold. Developers are now shifting from the concept stage to execution; use-cases have multiplied. The initial focus on the transport and steel sectors has widened into projects across dispatchable power, aviation, marine and long-duration energy storage. So far, few have reached final investment decision but the crystallisation of government support will change this. Larger proposals, however, will simply take time to secure sufficient offtake and financing, and will grapple with integration into the current energy system. Some developers will look to bring external capital in at the development stage including Big Oil.

Grid tech

Increased renewables penetration and electrification are driving changes to modernise grids. Transmission is the single biggest bottleneck in the power sector today, often forcing grid operators to curtail renewables from one location and dispatch higher cost power from elsewhere.

Dynamic line rating (DLR) leverages sensor and weather data to determine the real-time safe rating of the transmission line, allowing higher power throughput during favourable weather conditions. We expect the deployment of the technology can significantly reduce renewables curtailment and dispatch of fossil-fuel power generation.

Building automation system (BAS) enables centralised monitoring and control of loads within a commercial building, as well as advanced applications such as demand response. The BAS is the brain of a building, an enabler not only of smarter and more connected mechanicals and assets but of grid service capabilities, which are only beginning to be tapped.

Solar’s new growth phase

Solar’s dominance in renewables owes much to the low cost of ground mounted panels using Si-cells that are competitive with other sources of power in many markets. But the easy fruit has already been picked, with the best land locations nearing exhaustion. New module capacity expansions will adopt more efficient cells (n-type TOPCon cells with larger wafer formats). But solar’s next growth phase is about maximising land use. Floating solar, agrivoltaics and earth mount solar are some alternative means of implementing large-scale solar that aim either to decrease land use or piggyback solar onto existing applications on land or water. Wind power is moving in the same direction.

Nuclear

With variable renewables set to dominate power markets, there’s a pressing need for reliable, low-emissions baseload power. The nuclear industry’s comeback rests largely on small nuclear reactors (SMRs, maximum capacity of 300 MW). SMRs have a smaller geographical footprint, can better match offtakers’ needs and offer a degree of flexibility. Proponents also believe SMRs will end the industry’s poor project execution record.

Multiple SMR designs are competing, with reactors cooled respectively by water, gas, molten metal or molten salt. Large-scale nuclear is not out of the equation – Generation IV reactors (up to 1500 Mwe) are being designed with enhanced safety levels and minimal waste.

{kind=link}