Global power supply is on course to double by 2050 to meet surging demand as electrification gathers pace. Renewables will take the lion’s share of new capacity, wind and solar’s share of supply increasing from 10% today to over 50% by 2050 in our Base Case Energy Transition Outlook.

While renewables dominating power markets is an essential step on the road to net zero, high penetration of variable wind and solar exposes limitations in existing power systems. Brian Gaylord, Principal Analyst, talked me through Spain’s challenges, the latest in a growing list of global markets encountering teething problems as they adapt.

Dealing with variability

The build out of renewables to a material share of capacity has created problems in several markets around the world. The ‘duck curve‘ is a famous manifestation, describing the shape of power demand through the day net of solar and wind output. A system with high solar penetration will be ‘long’ power supply midday when the sun is shining and demand relatively modest; and ’short’ in the morning and evenings when demand is highest. Wholesale prices tend to follow the duck curve – lower prices during the day bookended by high prices when the system operator has to call on more expensive and flexible generation.

Renewables are by necessity often sited in locations of high wind or solar resource, away from demand centres. High wind production may be curtailed if there are transmission bottlenecks and insufficient demand, and curtailment can have a significant effect on prices. Systems in the US with nodal (local) pricing mechanisms can see negative prices where excess wind is being produced, and much higher prices in the demand centres where gas or coal plant has to be called on.

These effects are increasingly apparent in Europe. The Nordic market with its distinct pools of hydro power has also experienced price distortions. Germany in contrast has a single, national wholesale price but has major transmission bottlenecks between the north of the country where much of its wind power is generated and demand centres in the south.

Traders can cash in on these extreme events and their profits have to be paid for by someone. German consumers are thought to have forked out over EUR1 billion more on their bills last year due to curtailment. A political debate is underway in Germany whether introducing nodal pricing would send the right price signals to incentivise investment in transmission, improve the efficiency of the system, and give consumers a better deal.

Spain’s solar learning curve

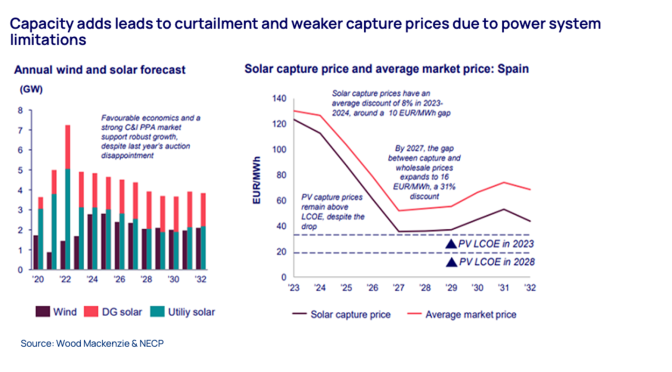

The Iberian market is one of the latest to experience renewables curtailment. A record 7GW of solar capacity was built in 2022, lifting renewables’ share of the market above 43% last year and to 55% in the first half of 2023. The additional solar output, near record wind output and high hydro levels all coincided with a fall in power demand of 4%. Inflexible nuclear output and minimal interconnection between Iberia and France added to the strain on the system.

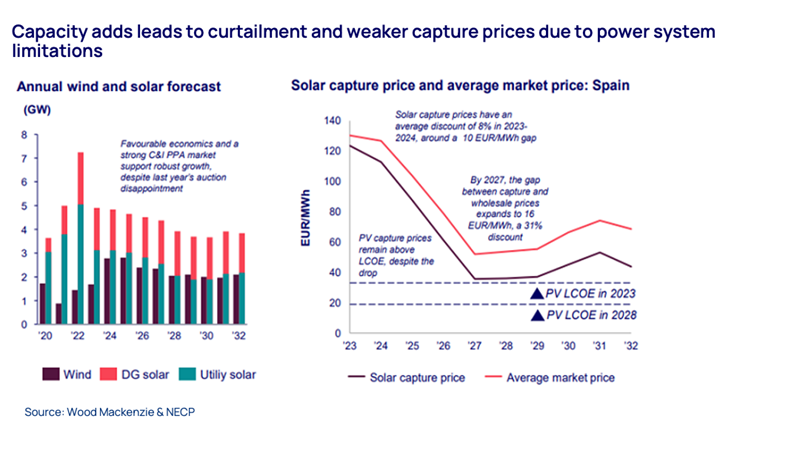

Solar output has been curtailed resulting in the erosion of prices. Solar capture prices have sunk to a material discount over the last eighteen months after broadly matching wholesale prices through 2021. And things will get worse before they get better – more solar and wind capacity additions over the next five years will lead to regular curtailment and weaker capture prices.

{kind=link}

The solutions – more transmission, more storage

Spain’s challenges should begin to ease by 2028 when nuclear retirals free up domestic transmission capacity; new export capacity to France starts to open up; and with demand growth driven by green hydrogen and heat pumps. Another key factor is substantial investment in battery and pump storage, with capacity expected to increase from 0.5 GW today to 9.3 GW by 2030. In future surplus renewables can be stored and sold into the market when it’s needed.

Markets that have been early adopters of renewables and have already reached a high penetration of wind and solar offer three valuable lessons to those in the early stages. First, renewables build-out needs to be integrated with adequate transmission capacity to move high volumes of renewables output to the demand centres. Second, energy storage, largely ignored until recently, is another key element. Storage twinned with renewables will allow any surplus power generated to be delivered when the market needs it – and at a reasonable cost to consumers.

Last, improved control of the demand side, both from grid edge technologies and the inherent storage capacity that will come from the coming ramp up of the electric vehicle stock.

Simon Flowers

Chairman, Chief Analyst and author of The Edge

Brian Gaylord

Principal Analyst, Global Power & Renewables