In the second week of December, prices in most markets were lower than in the previous week. A mostly lower electricity demand combined with a second consecutive week of lower gas and CO2 futures prices, and increased solar energy production in most of the major European electricity markets led to the downward trend.

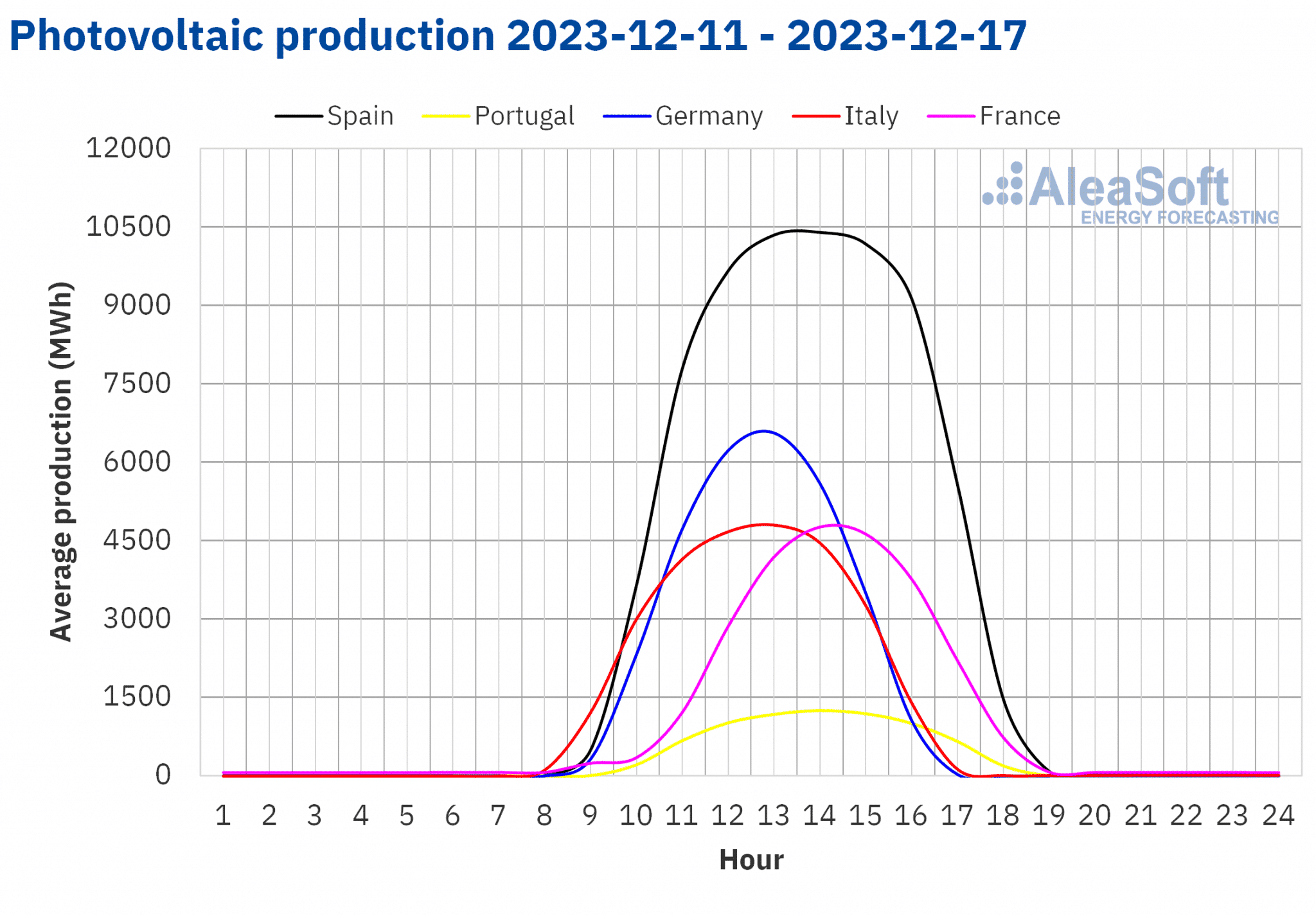

Concentrayed Solar Power, photovoltaic and wind energy production

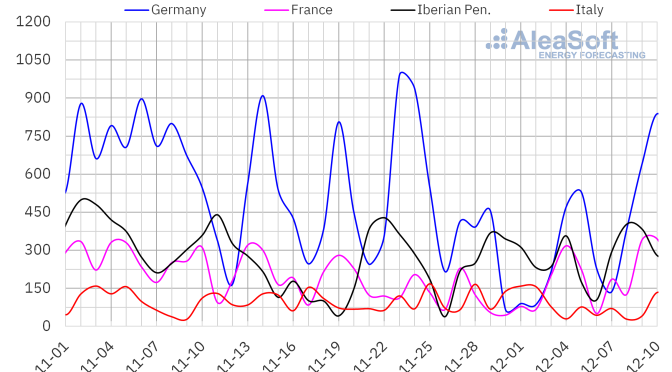

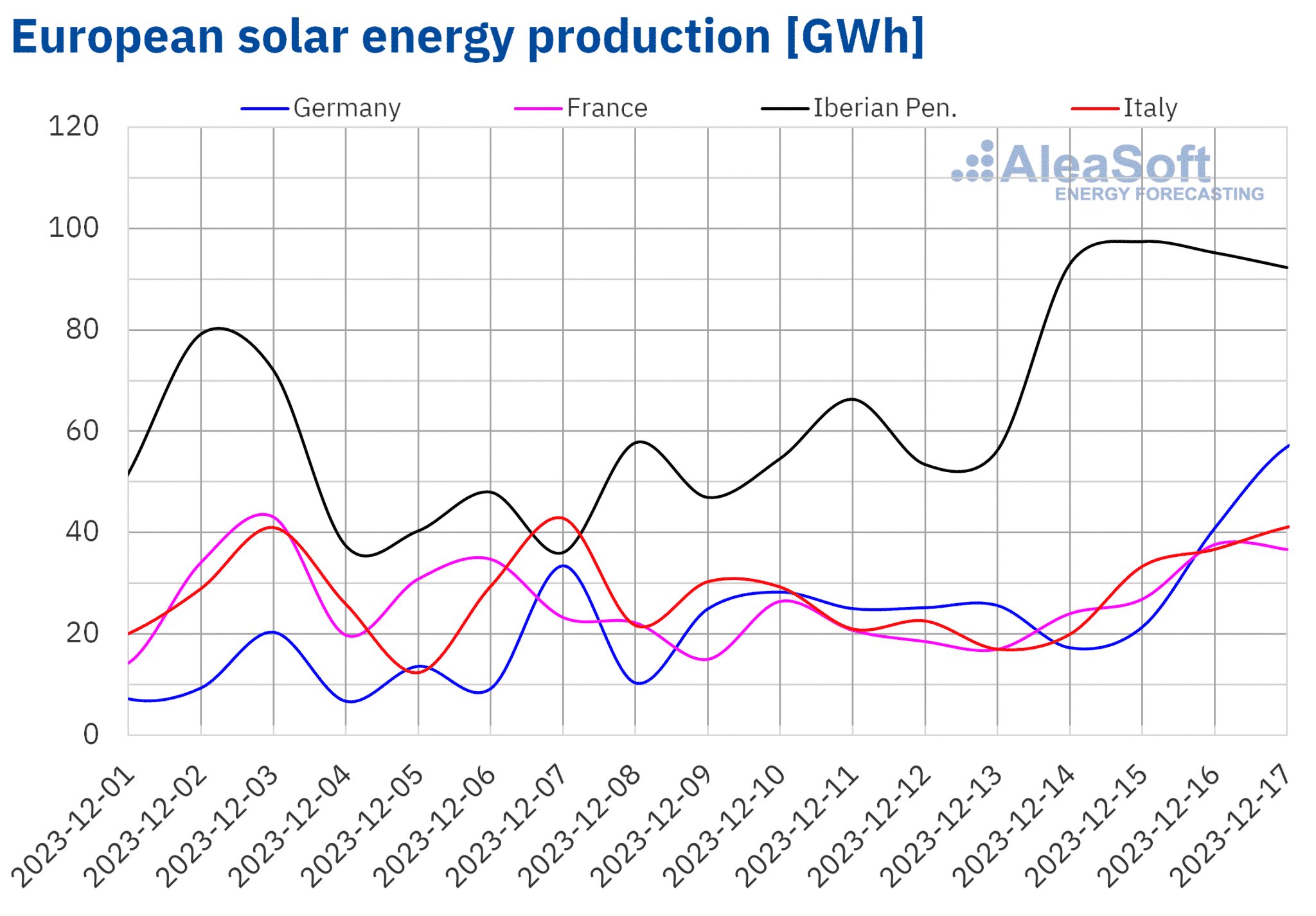

In the week of December 11, solar energy production increased in the major European electricity markets compared to the previous week. The increase ranged from 97% in Portugal to 5.3% in France. The exception was the Italian market, where solar energy production decreased by 0.1%.

AleaSoft Energy Forecasting‘s solar energy production forecasts indicate that production will increase in Germany, Italy and Spain during the week of December 18.

Source: Prepared by AleaSoft Energy Forecasting using data from ENTSO-E, RTE, REN, REE and TERNA.

Source: Prepared by AleaSoft Energy Forecasting using data from ENTSO-E, RTE, REN, REE and TERNA.

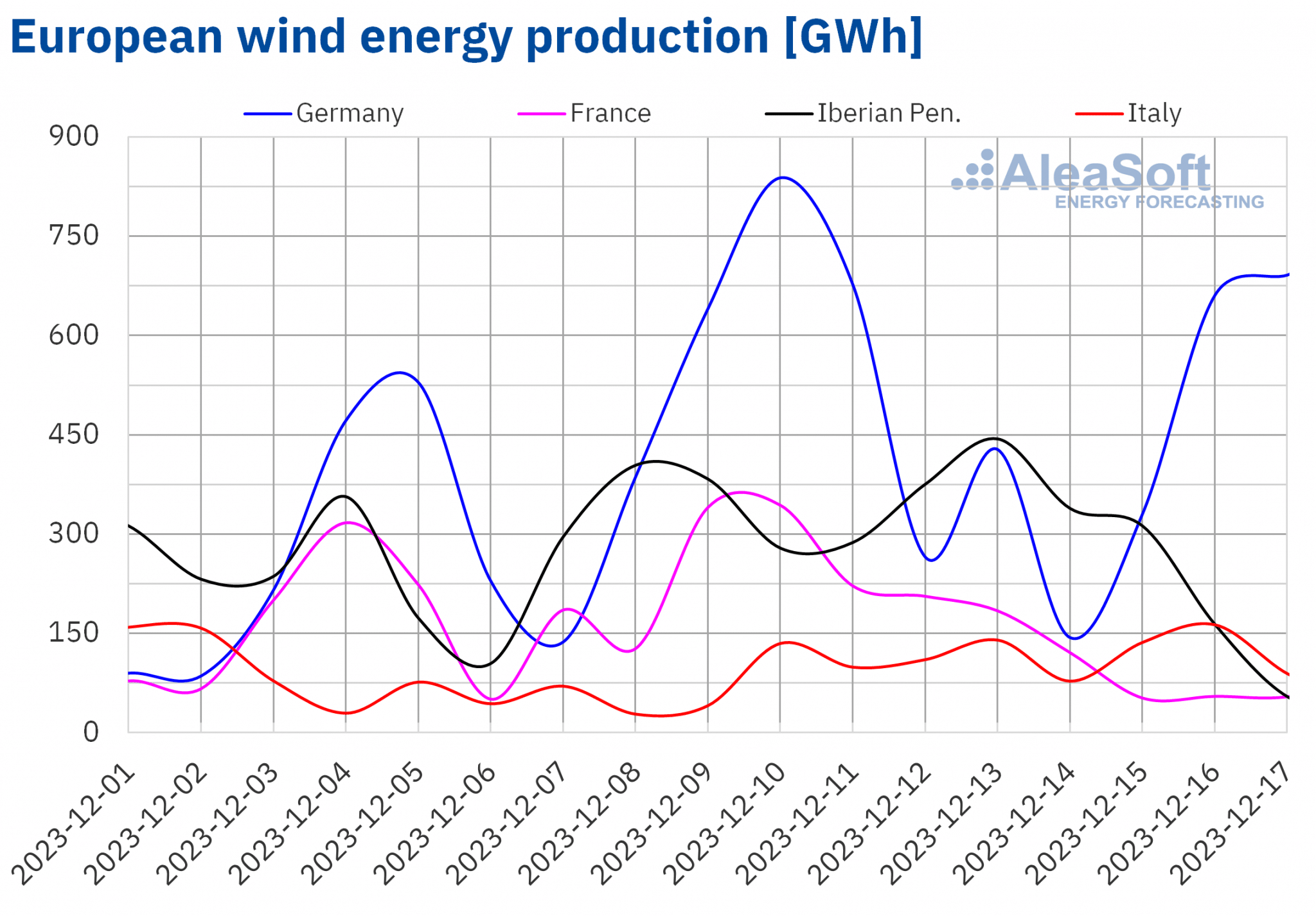

In the week of December 11, wind energy production decreased in the major European electricity markets compared to the previous week. The French market experienced the largest decrease with 44%. The Iberian Peninsula and German markets saw decreases of around 1.0%. As with solar energy production, the Italian market was the exception. There, wind energy production increased by 92% with an output of 817 GWh, the third highest weekly production.

AleaSoft Energy Forecasting‘s wind energy production forecasts indicate an increase in production for the French and German markets for the week of December 18, while a decrease is expected for the rest of the analyzed markets.

Source: Prepared by AleaSoft Energy Forecasting using data from ENTSO-E, RTE, REN, REE and TERNA.

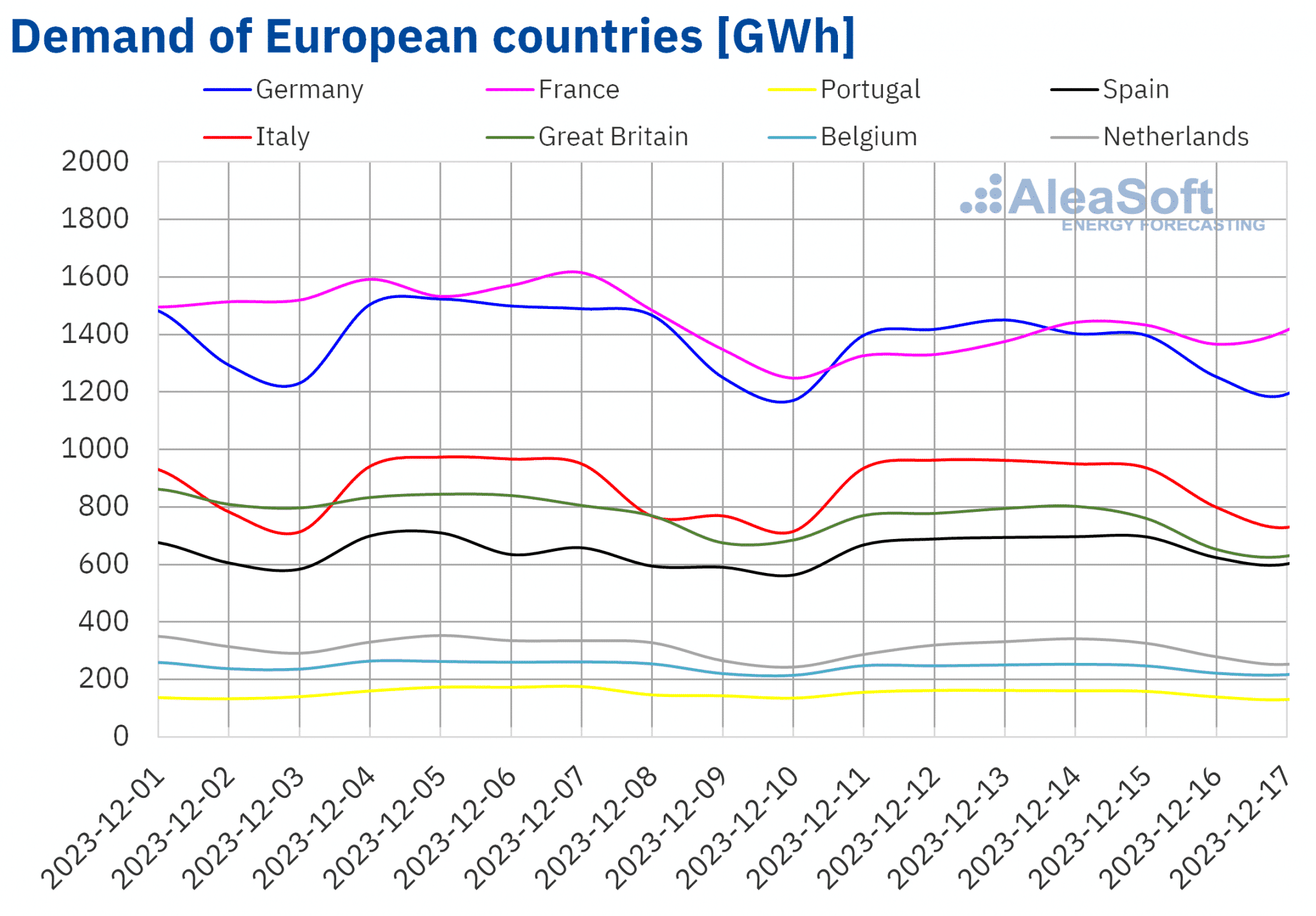

Electricity demand

During the week of December 11, electricity demand decreased in most major European electricity markets compared to the previous week. The decline in demand ranged from 6.7% in France to 2.3% in the Netherlands. The exceptions were the Spanish and Italian markets, where demand increased by 4.9% and 3.1% respectively. The recovery in demand was linked to the holidays of December 6, Constitution Day in Spain, and December 8, the Feast of the Immaculate Conception, celebrated in both countries.

The drop in demand was related to higher average temperatures compared to the previous week. Average temperature increases ranged from 4.7°C in Germany to 0.1°C in Portugal.

According to AleaSoft Energy Forecasting‘s demand forecasts for the week of December 18, electricity demand will decrease in the markets of Italy, Great Britain, Belgium and the Netherlands. On the other hand, an increase is expected in the markets of France, Portugal, Spain and Germany.

Source: Prepared by AleaSoft Energy Forecasting using data from ENTSO-E, RTE, REN, REE, TERNA, National Grid and ELIA.

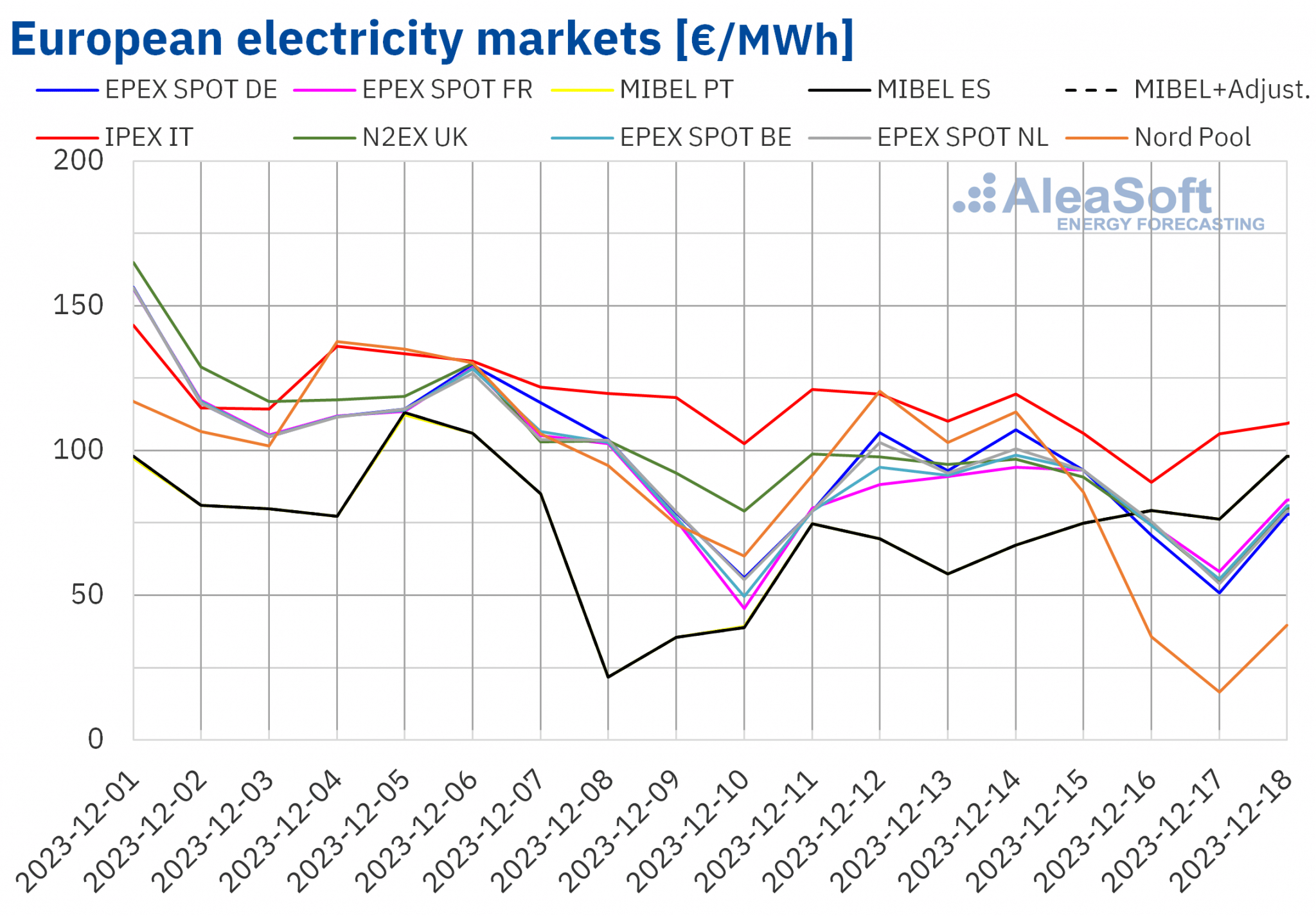

European electricity markets

During the week of December 11, prices in the major European electricity markets decreased compared to the previous week. The exceptions were the MIBEL market in Portugal and Spain with increases of 4.7% and 4.5% respectively. On the other hand, the Nord Pool market in the Nordic countries registered the largest price decrease with 24%, while the IPEX market in Italy registered the smallest decrease with 11%. In the rest of the markets analyzed by AleaSoft Energy Forecasting, prices fell between 14% in the EPEX SPOT market in the Netherlands and 18% in the N2EX market in the UK.

During the second week of December, most of the European electricity markets analyzed had weekly averages below €90/MWh. The exception was the Italian market with an average of €110.14/MWh. In contrast, the Spanish and Portuguese markets registered the lowest weekly averages of €71.30/MWh and €71.32/MWh, respectively. In the other markets analyzed, prices ranged from €80.85/MWh in the market of the Nordic countries to €86.95/MWh in the British market.

On the other hand, the Nordic market registered the highest hourly price of the second week of December, €162.04/MWh, on December 12, from 15:00 to 16:00. Throughout the week, prices on this market gradually decreased until reaching the lowest hourly price of €0.07/MWh on December 17, from 4:00 to 5:00.

During the week of December 11, the decrease in the average price of gas and CO2 emission rights and the decrease in electricity demand in most markets led to lower prices in most European electricity markets. Increased solar energy production in countries such as Germany and France also had a downward impact on prices.

AleaSoft Energy Forecasting‘s price forecasts indicate that prices could continue to fall in most major European electricity markets for the week of December 18. Increased solar energy production in markets such as the Italian and the German, along with increased wind energy production in Germany and France, could contribute to this behavior.

Source: Prepared by AleaSoft Energy Forecasting using data from OMIE, EPEX SPOT, Nord Pool and GME.

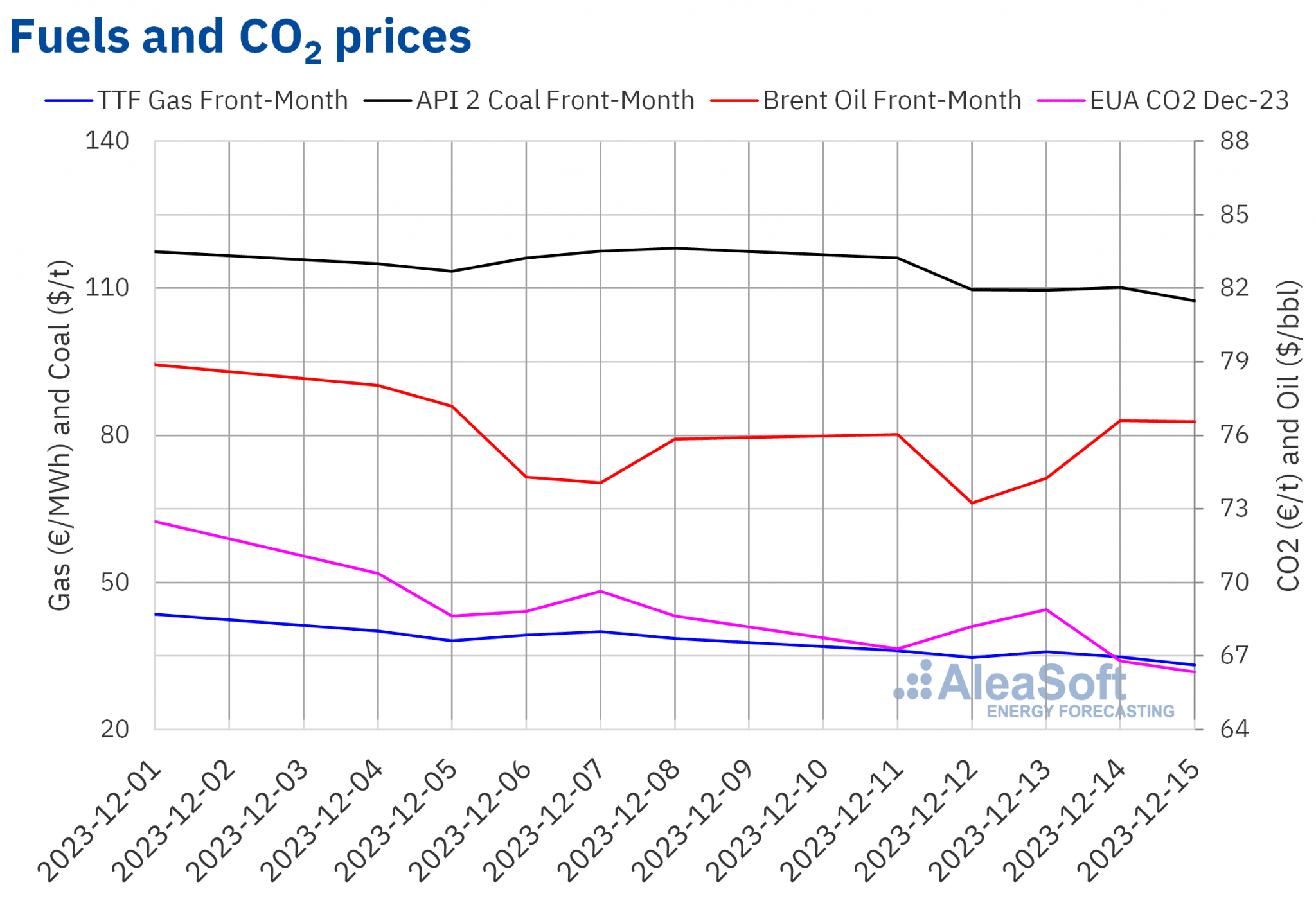

Brent, fuels and CO2

Brent oil futures for the Front-Month in the ICE market began Monday, December 11, with a slight increase of 0.3% from the previous week’s final session. However, on Tuesday, December 12, these futures registered their weekly minimum settlement at $73.24/bbl. This price was the lowest for the Front-Month since late June. After Tuesday’s decline, prices rebounded over the next two days, reaching a weekly high of $76.61/bbl on Thursday, December 14. Nevertheless, on Friday, December 15, prices fell 0.1% to $76.55/bbl.

Declining US crude oil inventories coupled with rising demand led to price increases in Brent oil futures during the second week of December. In addition, further production cuts agreed by OPEC+ also contributed to the price increases.

As for TTF gas futures in the ICE market for the Front-Month, they reached the maximum settlement price for the week of €36.12/MWh on Monday, December 11. This price was 6.4% lower than the last session of the previous week. On Tuesday, December 12, prices fell by 3.9% compared to the previous day to €34.70/MWh. Subsequently, on December 13, they recovered by 3.2% to reach €35.81/MWh, only to fall again in the following sessions to register the weekly minimum settlement price of €33.19/MWh on Friday, December 15. According to data analyzed by AleaSoft Energy Forecasting, this price was the lowest since the beginning of September.

In the second week of December, abundant supply and high European storage levels, as well as milder temperatures, led to further declines in TTF gas futures prices.

As for CO2 emission rights futures in the EEX market for the reference contract of December 2023, they experienced a decrease of 2.0% on Monday, December 11, compared to the last session of the previous week. On December 13, they reached their weekly maximum settlement price of €68.90/t, an increase of 1.0% compared to the previous day. In the days that followed, prices fell again to their weekly minimum settlement price of €66.35/t on Friday, December 15. This was the lowest price for that year’s December reference contract since October 2022.

Source: Prepared by AleaSoft Energy Forecasting using data from ICE and EEX.

AleaSoft Energy Forecasting’s analysis on the prospects for energy markets in Europe and the energy transition

Last Thursday, December 14, AleaSoft Energy Forecasting and AleaGreen held their last webinar of 2023. This edition marked the fourth anniversary since these webinars began to be held on a monthly basis. In the webinar, the speakers presented the services they offer to the energy sector and how they can serve the various players in the sector. They also discussed the evolution of the energy markets in 2023 and the prospects for 2024.

The first 2024 webinar, organized by AleaSoft Energy Forecasting and AleaGreen, will take place on January 18 and will feature speakers from PwC Spain for the fourth time. It will analyze the evolution of the European energy markets and the prospects from 2024 onwards, as well as the vision of the PPA market for consumers in the current context.