Demand in 2023 remained strong despite market disruptions by supply and inventory issues in the second half of the year. Shipment volumes of the list of manufacturers increased significantly, up by 78% YoY. There is a clear distinction among module makers, with top-ranked companies remained the same as the previous year, but the second-ranked companies shuffled markedly amid severe competition. The number of companies increased to 13 due to close shipment volumes of companies ranked 10th. The ranking is based on statistics from InfoLink’s database and InfoLink’s survey on manufacturers. Should there be any manufacturer yet to calculate its shipment volume, we use operational data and our estimation based on production output and inventory from the database. Also, manufacturers whose total shipment does not differ by more than 5% are tied for the rankings. Official figures shall prevail when there is any discrepancy.

Strong shipment volume, severe competition among second-ranked companies

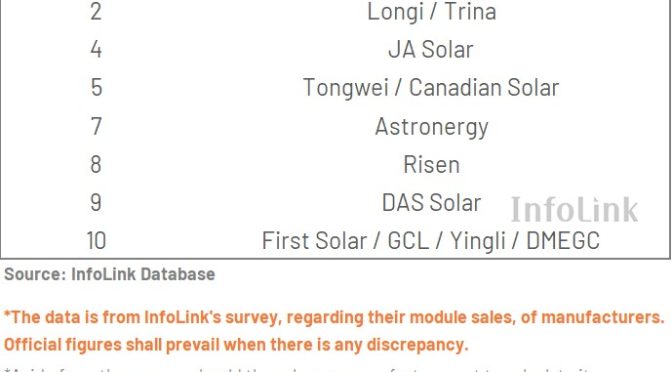

Jinko, Longi/Trina, and JA Solar secured the first to fourth places with a slight reshuffle. Since 2019, the biggest four vertically integrated companies have retained their positions. Clearly, the biggest companies are getting bigger in recent years, leaving the second-ranked ones behind with significant shipment gap. The gap stood at 20 GW between leading companies and those ranked from the fifth in 2022, and then the gap widened to 30 GW in 2023 with 60 GW difference between the first fourth and the rest. It’s estimated that the top four companies took up around 60% of the total shipments of the top-10 list.

The second-ranked companies experienced fierce competition. The ranking saw clear change, with Tongwei and Canadian Solar tied for the fifth place, followed by Astronergy and Risen. The lowest volume reached 20 GW among those ranked fifth to eighth.

DAS Solar was ranked ninth, followed by First Solar/GCL/Yingli/DMEGC that tied for the tenth. Older brands returned to the top-10 list this time, indicating the continuation of fierce competition into 2024.

Companies outside of the rankings, including Suntech, Solargiga, Q-Cells, Huansheng Solar and Seraphim, saw shipment volume rising to 7-10 GW.

Highlights of 2023 shipment rankings

Jinko: With advantage in choosing n-type technology early, the company has posted strong shipment volume in the first half, increasing by 74% from 2022, and thus reclaiming the top.

Longi: Stable performance kept the company in the second place. It has achieved GW-scale shipment of HPBC products, but a slightly slower annual growth rate than the top four companies, sitting at 48%.

Trina: The company’s shipment volume differed less than 5% from Longi and thus they were tied for the second. It’s worth noting that Trina’s advantage in rectangle wafers and long-term engagement in G12R product series allowed it to reach an annual growth rate of 55%, a stellar performance.

JA Solar: With stable business planning, cost management and overseas channel management, it has long been on the top four list. Its shipment grew steadily, with 46% annual growth rate.

Tongwei: With advantages across the supply chain, the company has climbed from the second-ranked in 2022 to the middle and posted an annual growth rate as high as 262% compared with 2022. Tongwei was also the only company that entered both the cell and module rankings.

Canadian Solar: Following its stable operation principle, the company has stayed on the middle of the list for more than five years. Its market share of overseas shipment topped the list this time.

Astronergy: The company’s annual growth rate reached 108%, with its domestic market share rising noticeably. Meanwhile, the company’s long-term engagement in n-type products enabled it to secure the second largest share of n-type shipments.

Risen: While its annual growth rate slowed this time, its strategy of offering diverse products made it the only company that shipped both n-type TOPCon and HJT products on the list.

DAS Solar: As a new entrant to n-type field in recent years, the company has come close to the top-10 list in 2022, and climbed to the ninth place this time. It secured the fifth place in terms of n-type TOPCon shipment, with its annual growth rate hitting 113%.

First Solar: It’s the only non-China company on the ranking. Since its entry to the list in 2020, the company has sustained a shipment volume between at least 6 GW to 9 GW. Its annual growth rate is expected to reach 29% this year. With a focus in the US market, the company’s overall profitability is strong.

GCL: The company was one of the top-10 in the past but had fallen outside of the list in 2019, but re-entered the list in 2023. Domestically, its shipment volume accounted for the highest share in China, having secured large orders from state-owned companies. Its annual growth rate stood at 494%, the highest of all.

Yingli: An old brand that has been focusing on the domestic market and exploring overseas channels in recent years. According to information available, the company secured a leading position in the list of awarded companies in China’s auctions last year, with more than 100% annual growth rate in shipments.

DMEGC: The company has been focusing on Europe’s distributed generation market and France’s low-carbon module market, securing a second position in the market share of overseas shipment and posted an annual growth rate as high as 134%. The company is planning to scale up its business in domestic and overseas markets, as well as distributed generation market.

Market share of domestic shipment continues to grow

First Solar aside, the average share of shipment to non-China markets in 2022 was around 50-55%; the figure declined to 40-45% in 2023, a downward trend for two consecutive years.

Rationale behind included inventory pileup in overseas markets and sluggish economy, but the major reason was that companies that returned to the list or new entrants have relatively weaker overseas channels than the top four largest brands, while growing domestic market underpinned demand. These factors led to a decrease in the share of shipment to non-China markets.

Large size and n-type products dominate shipments

Among the PERC products (including rectangle wafers) shipped by the top 10 companies (excluding First Solar), the share of M10 (18Xmm) and G12 reached 70%, of which G12 and G12R accounted for 22%. The share of M6 (166mm) and other sizes of PERC fell to only 2%. Module shipments of n-type TOPCon (all sizes) rose markedly to 26%.

Shipment targets remain ambitious for 2024

Looking ahead, the total shipment is estimated to reach 700 GW based on the shipment targets of companies on the list. Of which, the share of products of new technology accounts for more than 70%; some even plan for 90-100%, with TOPCon the majority. The top four largest companies’ shipment target is raised to beyond 90 GW level and even 120 GW, leaving the second-ranked companies behind.

InfoLink projects that module demand growth will slow this year, sitting at 460-519 GW with only 11% of annual growth rate. With a total planned shipment volume of 700 GW by the top 10 companies, the competition will remain fierce this year.

Impact of surplus supply has emerged, with acceptance rate diversifying markedly in the first quarter of this year. Amid the competition manufacturers shall make decision fast, differentiating products, and securing technology advantage. Module power output, quality, and efficiency will be key factors determining manufacturers’ competitiveness edge this year. Meanwhile, overseas market movements, especially policy changes and conditions on materials use and product of origin, should be closely monitored, as preparing in advance will be key to stand out of the severe competition for manufacturers.