In the second week of March, prices in European electricity markets showed few variations compared to the previous week, except in the MIBEL market, where they doubled. Even so, the Iberian Peninsula registered the lowest prices. Photovoltaic energy production in Spain and Portugal reached the levels of the end of August and set another record for a March month. Wind energy production fell in most markets. On March 14, Brent futures reached their highest price since early November, $85.42/bbl.

Solar photovoltaic, solar thermoelectric and wind energy production

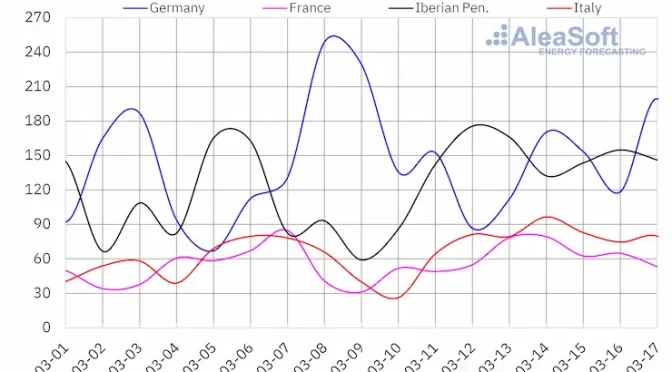

In the week of March 11, solar energy production increased in most major European electricity markets compared to the previous week. The Spanish market reached the largest increase, 48%, reversing the downward trend of the previous week. The French market registered the smallest increase, 12%, rising for the third consecutive week. The German market was an exception to the upward trend. In this market, after four weeks of increases, solar energy production fell by 2.5%.

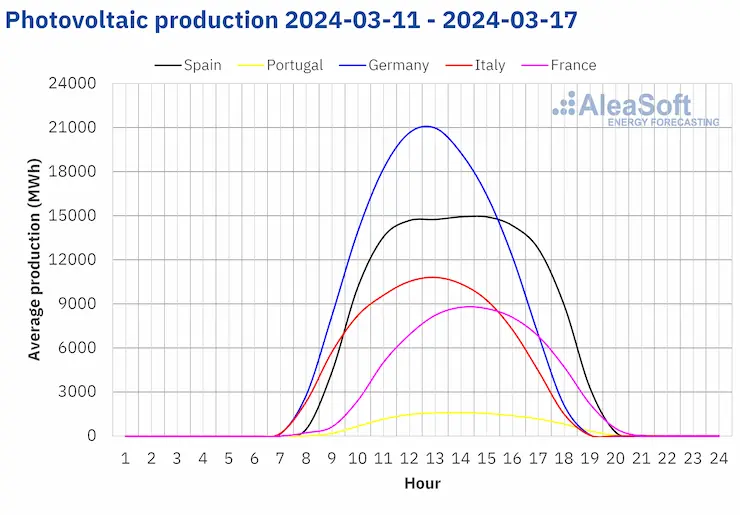

In the Iberian Peninsula, the highest solar photovoltaic energy production records for a March month were broken again. On the 12th, the Spanish and Portuguese markets produced 143 GWh and 14 GWh, respectively. These production levels were last registered at the end of August.

For the week of March 18, according to AleaSoft Energy Forecasting’s solar energy production forecasts, the trend registered in the previous week will be reversed. Solar energy production will increase in Germany but it will decrease in Spain and Italy.

Source: Prepared by AleaSoft Energy Forecasting using data from ENTSO-E, RTE, REN, REE and TERNA.

Source: Prepared by AleaSoft Energy Forecasting using data from ENTSO-E, RTE, REN, REE and TERNA.

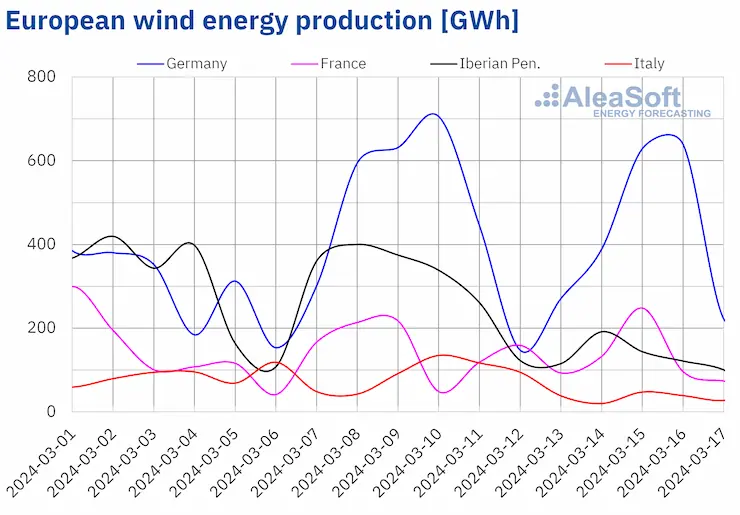

In the week of March 11, wind energy production decreased in most major European electricity markets compared to the previous week. The Portuguese market registered the largest decline, 61%, continuing the downward trend of the previous week. The German market registered the smallest decline, 4.9%, reversing the previous week’s increase. On the other hand, wind energy production in France increased by 1.1%, also reversing the previous week’s trend.

For the week of March 18, AleaSoft Energy Forecasting’s wind energy production forecasts predict that the trends registered in most markets during the week of March 11 will reverse. Wind energy production will increase in the Iberian Peninsula and Italy and it will decrease in Germany and France.

Source: Prepared by AleaSoft Energy Forecasting using data from ENTSO-E, RTE, REN, REE and TERNA.

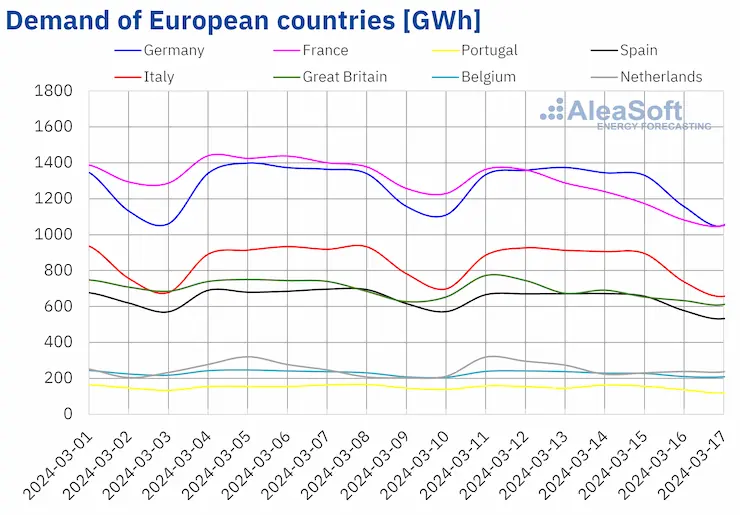

Electricity demand

In the week of March 11, electricity demand fell on a week?on?week basis in most major European electricity markets, continuing the downward trend of the previous week. The French market, where demand fell for the second consecutive week, registered the largest decline, 11%. The Belgian market registered the smallest decline, 1.2%, also for the second consecutive week. The Dutch market was the exception to the downward trend. In this market, after four weeks of decline, demand increased by 4.1%.

At the same time, average temperatures increased in all analyzed European markets. Increases ranged from 1.1 °C in Italy to 3.3 °C in Portugal.

For the week of March 18, according to AleaSoft Energy Forecasting’s demand forecasts, the downward trend will continue in France, Spain, Italy and Belgium. In contrast, demand will increase in Germany, Portugal, Great Britain and the Netherlands.

Source: Prepared by AleaSoft Energy Forecasting using data from ENTSO-E, RTE, REN, REE, TERNA, National Grid and ELIA.

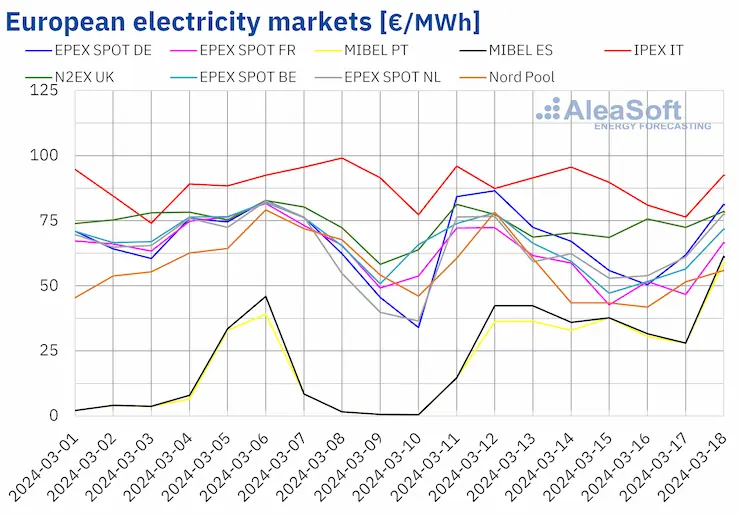

European electricity markets

During the week of March 11, average prices in most major European electricity markets remained little changed from the previous week. The exception was the MIBEL market of Spain and Portugal. After registering weekly prices below €15/MWh in the first week of March, in the week of March 11, it reached the highest percentage price rises again, with weekly averages exceeding €30/MWh. The Spanish market average increased by 136% and the Portuguese market, by 141%. Weekly prices also rose in the N2EX market of the United Kingdom and in the EPEX SPOT market of the Netherlands and Germany, with increases of 0.6%, 1.0% and 5.9%, respectively. In the rest of the markets analyzed at AleaSoft Energy Forecasting, prices declined between 2.5% in the IPEX market of Italy and 15% in the Nord Pool market of the Nordic countries.

In the second week of March, weekly averages were below €65/MWh in most analyzed European electricity markets. The exceptions were the German market, the British market and the Italian market, with averages of €68.34/MWh, €73.50/MWh and €88.23/MWh, respectively. On the other hand, despite the increases, the Portuguese and Spanish markets registered the lowest weekly prices again, which were €30.89/MWh and €33.24/MWh, respectively. In the rest of the analyzed markets, prices ranged from €54.23/MWh in the Nordic market to €63.24/MWh in the Dutch market.

Regarding hourly prices, in the second week of March, only the Iberian market registered prices below €1/MWh, despite the increase in its weekly average price. Most of these prices occurred on Monday, March 11. On that day, the MIBEL market registered thirteen hours with a price of €0/MWh, under the influence of high levels of wind energy production in Spain.

During the week of March 11, the decline in the average price of gas and CO2 emission rights exerted a downward influence on European electricity market prices. Electricity demand also fell in most analyzed markets. On the other hand, the fall in wind energy production led to higher prices in markets such as the Iberian market or the German market, where solar energy production also fell.

AleaSoft Energy Forecasting’s price forecasts indicate that in the third week of March prices might follow the same trend of the current week in most analyzed European electricity markets.

Source: Prepared by AleaSoft Energy Forecasting using data from OMIE, EPEX SPOT, Nord Pool and GME.

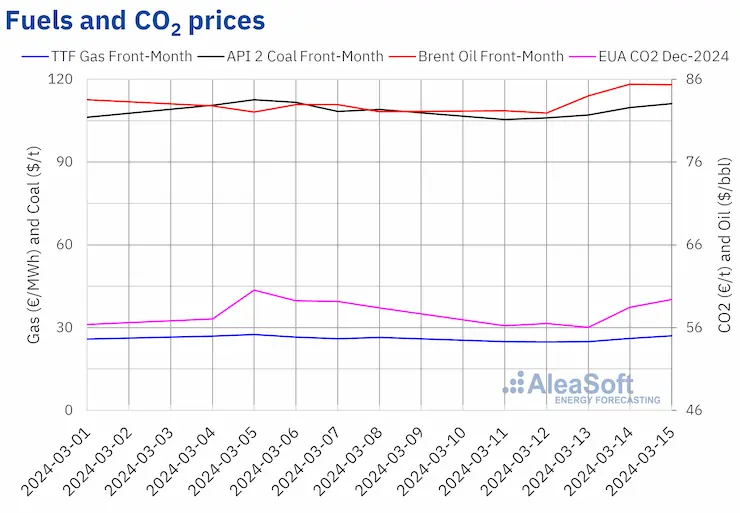

Brent, fuels and CO2

Settlement prices of Brent oil futures for the Front?Month in the ICE market registered price increases in most sessions of the second week of March. However, on Tuesday, March 12, with a slight decrease from Monday, these futures reached their weekly minimum settlement price, $81.92/bbl. On the other hand, as a result of the registered increases, on Thursday, March 14, they reached their weekly maximum settlement price, $85.42/bbl. According to data analyzed at AleaSoft Energy Forecasting, this price was 3.0% higher than the previous Thursday and the highest since early November 2023. On Friday, the settlement price was back down slightly to $85.34/bbl, still 4.0% higher than the previous Friday.

In the second week of March, the International Energy Agency revised upwards its oil demand forecast for 2024, which led to settlement prices above $85/bbl in the last sessions of the week. OPEC+ production cuts and the drop in oil stocks of the United States also contributed to this behavior.

As for TTF gas futures in the ICE market for the Front?Month, settlement prices remained below €25/MWh in the first three sessions of the second week of March. These futures registered their weekly minimum settlement price, €24.77/MWh, on Tuesday, March 12. According to data analyzed at AleaSoft Energy Forecasting, this price was 9.8% lower than the previous Tuesday and the lowest since the end of February. As of Wednesday, March 13, prices started to rise until they reached their weekly maximum settlement price, €27.03/MWh on Friday, March 15. This settlement price was 2.4% higher than the previous Friday.

In the second week of March, supply concerns continued due to disruptions in exports from the Freeport liquefied natural gas plant in the United States. Forecasts of wind energy production declines in part of Europe and increased demand in Asia also contributed to TTF gas futures prices increases. However, European reserve levels prevented further price rises.

As for settlement prices of CO2 emission rights futures in the EEX market for the reference contract of December 2024, they started the second week of March with declines and they remained below €57/t until Wednesday. On that day, these futures registered their weekly minimum settlement price, €56.04/t. According to data analyzed at AleaSoft Energy Forecasting, this price was 5.4% lower than the previous Wednesday and the lowest in the first half of March. In the remaining sessions of the second week of March, prices increased. As a result, on Friday, March 15, the settlement price was €59.39/t, 1.7% higher than on the previous Friday.

Source: Prepared by AleaSoft Energy Forecasting using data from ICE and EEX.

AleaSoft Energy Forecasting’s analysis on the prospects for energy markets in Europe and the energy transition

The third webinar of 2024 of AleaSoft Energy Forecasting and AleaGreen took place on Thursday, March 14. This webinar was the 42nd in their monthly webinar series and it featured guest speakers from EY for the fourth time. In addition to the prospects for European energy markets, the webinar analyzed regulation, financing of renewable energy projects, PPA, self?consumption, portfolio valuation, the green hydrogen auction and the Innovation fund.

AleaSoft Energy Forecasting and AleaGreen will hold their next webinar on April 11. On this occasion, the webinar will focus on energy storage and it will have the participation, for the third time, of Raúl García Posada, Director at ASEALEN, the Spanish Energy Storage Association.