In the week of April 29, prices in the main European electricity markets fell compared to the previous week. The exception was the Iberian MIBEL market, where prices rose, although they were the lowest again for the thirteenth consecutive week. Most markets registered negative hourly prices. Portugal and Italy broke the historical records for solar photovoltaic energy production over the weekend. Also in Italy, wind energy reached a record for a May month on the 3rd. Electricity demand fell in all markets.

Solar photovoltaic, solar thermoelectric and wind energy production

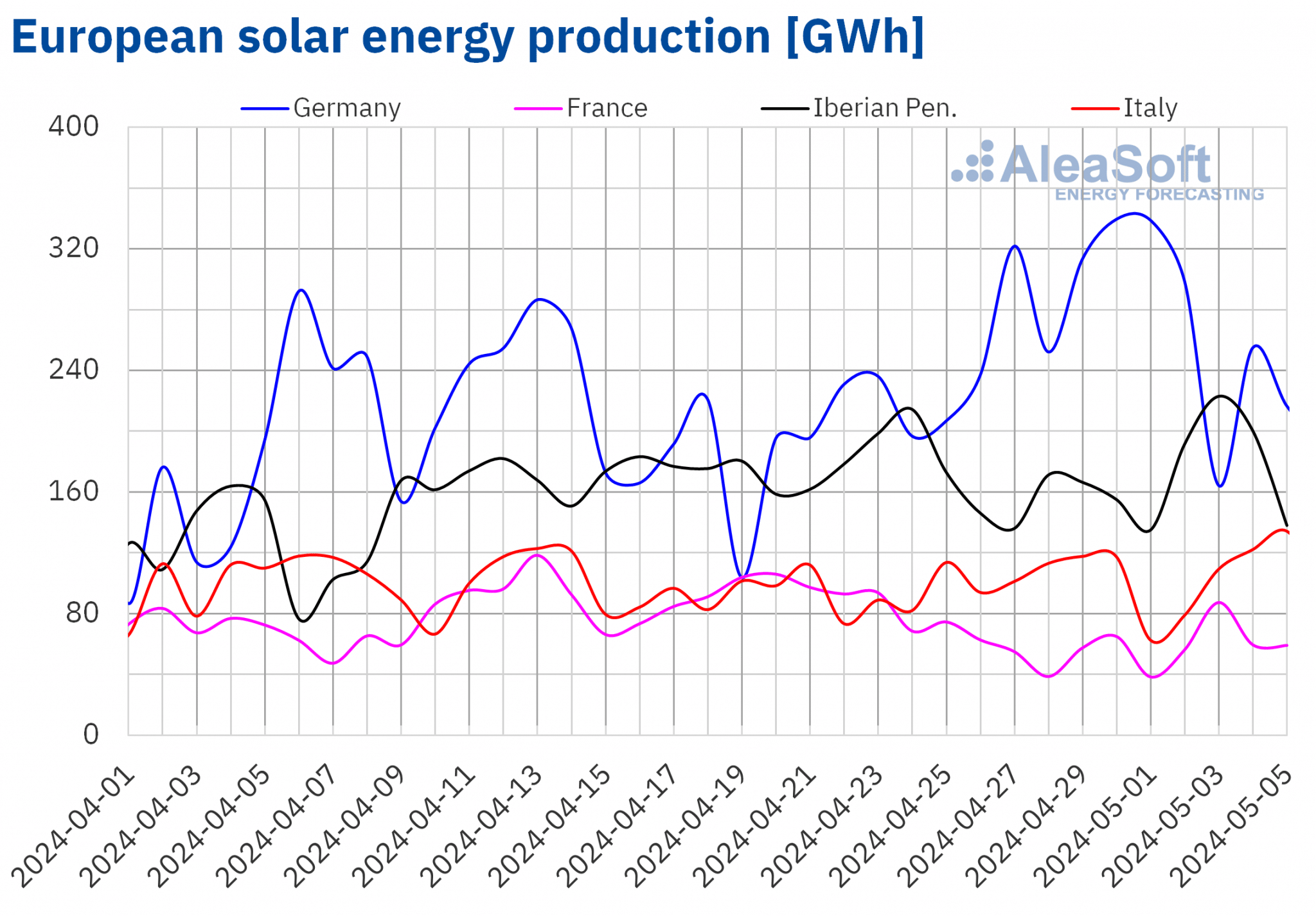

In the week of April 29, solar energy production increased in the German and Italian markets for the second consecutive week. The German market registered the largest increase, 15%, while in the Italian market the increase was 11%. On the other hand, in the French and Portuguese markets, solar energy production fell by 13% and 8.0%, respectively. In the Spanish market, solar energy production, which includes photovoltaic and thermoelectric energy, fell by 0.5%, breaking the upward trend registered over the last four weeks.

Despite the overall lower solar energy production in Portugal during the first week of May, on Saturday, May 4, the historical record for daily solar photovoltaic energy production was broken again, with 18 GWh. The Italian market also set an all?time record for production using this technology one day later, on Sunday, May 5, with 134 GWh of solar photovoltaic energy generation.

For the week of May 6, according to AleaSoft Energy Forecasting’s solar energy production forecasts, it will decrease in Italy and Spain. However, solar energy production will continue to increase in Germany.

Source: Prepared by AleaSoft Energy Forecasting using data from ENTSO-E, RTE, REN, REE and TERNA.

Source: Prepared by AleaSoft Energy Forecasting using data from ENTSO-E, RTE, REN, REE and TERNA.

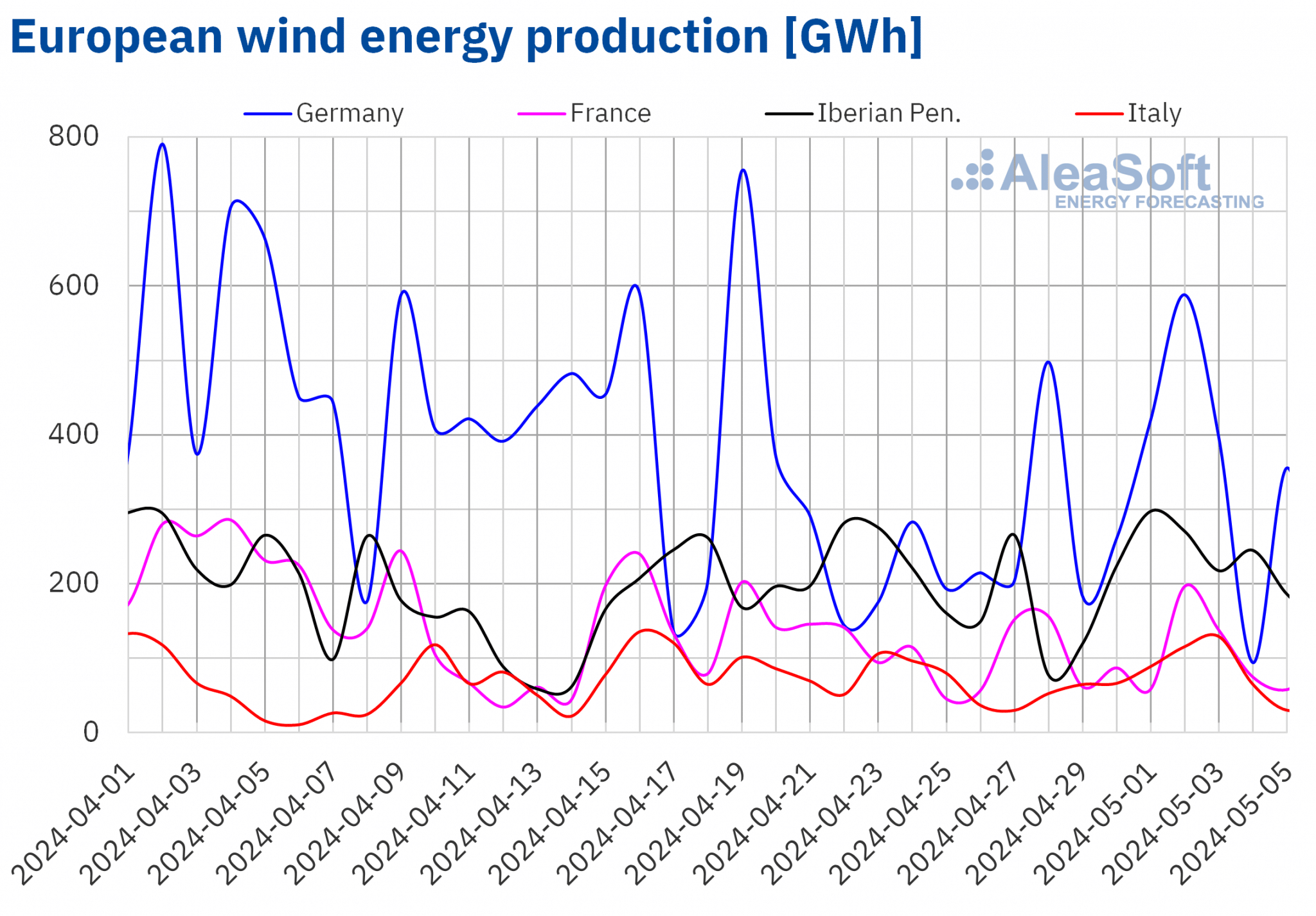

In the first week of May, wind energy production increased in most major European markets compared to the previous week. The German market registered the largest increase, 34%, reversing the downward trend of the last three weeks. In the Italian market, the increase was 24%, followed by increases of 17% and 7.2% in the Portuguese and Spanish markets, respectively. Portugal has registered an increase in wind energy production over the last three weeks. On the other hand, the French market registered declines for the second consecutive week, this time by 11%.

During the week of April 29, the Italian market broke the all?time record for daily wind energy production for a May month, with 129 GWh generated using this technology on Friday, May 3.

In the second week of May, according to AleaSoft Energy Forecasting’s wind energy production forecasts, it will decline in all analyzed markets.

Source: Prepared by AleaSoft Energy Forecasting using data from ENTSO-E, RTE, REN, REE and TERNA.

Electricity demand

In the week of April 29, electricity demand decreased in all major European electricity markets compared to the previous week. The French and British markets registered the largest declines, 13% and 10% respectively. In the German, Belgian, Spanish and Italian markets, demand declines ranged from 7.3% in the German market to 3.2% in the Italian market. In the Italian market, demand continued the downward trend of the last three weeks, while in Germany and Belgium it was the second consecutive week with this trend. In the market of the Netherlands, the decrease in demand was 0.4%. The Portuguese market continued to register declines in demand for the fifth consecutive week, this time by 0.1%, which was the smallest decline of the week compared to the rest of the analyzed markets.

The drop in demand in European markets during the first week of May was largely related to the May 1 holiday, International Workers’ Day, which was celebrated in most Europe. Increases in average temperatures in most markets also contributed to the decline in demand. In Great Britain, Belgium, the Netherlands and Germany, average temperatures increased between 4.2 °C and 8.3 °C. In Spain, France and Italy, the increases were smaller, ranging from 1.6 °C to 4.2 °C. Portugal was the exception, with average temperatures decreasing by 0.9 °C.

For the second week of May, according to AleaSoft Energy Forecasting’s demand forecasts, electricity demand will increase in the Italian and Spanish markets. On the other hand, in the markets of France, Great Britain, Belgium, Germany, the Netherlands and Portugal, demand will continue to decrease.

Source: Prepared by AleaSoft Energy Forecasting using data from ENTSO-E, RTE, REN, REE, TERNA, National Grid and ELIA.

European electricity markets

In the first week of May, prices in the main European electricity markets fell compared to the previous week. The exception was the MIBEL market of Spain and Portugal, with rises of 11% and 13%, respectively. The EPEX SPOT market of France and the Nord Pool market of the Nordic countries reached the largest percentage price declines, 44% and 49%, respectively. In contrast, the N2EX market of the United Kingdom registered the smallest percentage decline, 6.8%. In the rest of the markets analyzed at AleaSoft Energy Forecasting, prices fell between 17% in the EPEX SPOT market of the Netherlands and 27% in the EPEX SPOT market of Germany and Belgium.

In the first week of May, weekly averages were below €65/MWh in most analyzed European electricity markets. The exceptions were the British market and the IPEX market of Italy, with averages of €80.48/MWh and €82.83/MWh, respectively. The Spanish and Portuguese markets registered the lowest weekly averages, €28.33/MWh and €28.34/MWh, respectively, for the thirteenth consecutive week. In the rest of the analyzed markets, prices ranged from €33.84/MWh in the French market to €61.53/MWh in the Dutch market.

Regarding hourly prices, most analyzed European markets registered negative prices on May 1 and 5. The exceptions were the British, Italian and Nordic markets. The German, Belgian and Dutch markets also registered negative prices on May 2. The Dutch market reached the lowest hourly price, ?€200.00/MWh, on Wednesday, May 1, from 13:00 to 15:00. This price was the lowest in this market since the beginning of July 2023.

During the week of April 29, the fall in demand, a slight decrease in the average gas price and the increase in wind energy production in most analyzed markets had a downward influence on European electricity market prices. In the case of the German and Italian markets, moreover, solar energy production increased.

AleaSoft Energy Forecasting’s price forecasts indicate that prices might increase in most analyzed European electricity markets in the second week of May, influenced by the drop in wind energy production. In addition, solar energy production might decrease in markets such as Spain and Italy.

Source: Prepared by AleaSoft Energy Forecasting using data from OMIE, EPEX SPOT, Nord Pool and GME.

Brent, fuels and CO2

Settlement prices of Brent oil futures for the Front?Month in the ICE market fell during the first week of May. On Monday, April 29, these futures reached their weekly maximum settlement price, $88.40/bbl. This price was 1.6% higher than the previous Monday. However, as a result of the downward trend of the first week of May, on Friday, May 3, they registered their weekly minimum settlement price, $82.96/bbl. According to data analyzed at AleaSoft Energy Forecasting, this price was 7.3% lower than the previous Friday and the lowest since the first half of March.

During the first week of May, concerns about the evolution of the world economy and its effects on demand caused Brent oil futures prices to fall. High inflation levels in the United States might delay the lowering of interest rates in the country. On the other hand, expectations of a ceasefire in Gaza also contributed to the price decline. However, in the second week of May, the possibility of OPEC+ maintaining its production cuts after June and the worsening conflict in the Middle East might exert an upward influence on prices.

As for TTF gas futures in the ICE market for the Front?Month, on Monday, April 29, they reached their weekly minimum settlement price, €27.99/MWh. According to data analyzed at AleaSoft Energy Forecasting, this price was 5.8% lower than the previous Monday and the lowest in the second half of April. In the following two sessions of the first week of May, settlement prices remained below €30/MWh. However, on Thursday, May 2, after a 7.6% rise over the previous session, these futures reached their weekly maximum settlement price, €30.91/MWh. This price was 3.8% higher than the previous Thursday. In the last session of the first week of May, the settlement price was €30.53/MWh.

In the first week of May, prospects for an improvement in the Middle East conflict and high European reserves levels exerted their downward influence on TTF gas futures prices. However, forecasts of declines in wind energy production contributed to the recovery in prices at the end of the week.

As for CO2 emission allowances futures in the EEX market for the reference contract of December 2024, settlement prices remained below €70/t in the last two sessions of April. On Monday, April 29, these futures reached their weekly minimum settlement price, €65.49/t. According to data analyzed at AleaSoft Energy Forecasting, this price was 1.3% lower than the previous Monday and the lowest in the second half of April. In contrast, on Thursday, May 2, these futures registered their weekly maximum settlement price, €72.52/t. This price was 6.0% higher than the previous Thursday. The settlement price for the last session of the first week of May was €72.01/t. Despite the slight decrease from the previous day, this price was still 7.6% higher than the previous Friday.

Source: Prepared by AleaSoft Energy Forecasting using data from ICE and EEX.

AleaSoft Energy Forecasting’s analysis on the prospects for energy markets in Europe and the energy transition

Next Thursday, May 9, AleaSoft Energy Forecasting and AleaGreen will hold the 44th webinar of their monthly webinar series. The topics of this webinar will be the evolution and prospects of European energy markets, low, zero and negative prices in European electricity markets, the vision of the future of the energy sector and the energy transition vectors, such as renewable energy, demand, energy storage and green hydrogen. The analysis table of the webinar in Spanish will count with the participation, for the second time, of Luis Atienza Serna, Minister of the Spanish Government between 1994 and 1996 and president of Red Eléctrica de España between 2004 and 2012.