Wind turbine manufacturers supplied a record amount of volume in 2023, according to GWEC’s annual Supply Side Data report. GWEC Market Intelligence found a total of 30 wind turbine manufacturers installed a record 120.7 GW of new capacity last year, despite a challenging macroeconomic environment and continuing supply chain challenges.

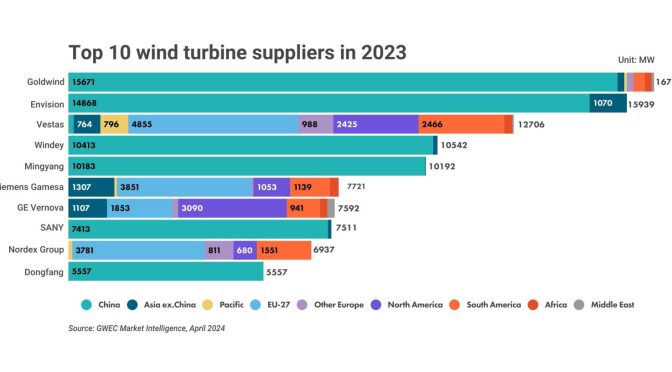

Chinese suppliers installed 81.6 GW in 2023, resulting in Chinese companies occupying four of the top five spots in this year’s supplier rankings. Goldwind emerged as top supplier in 2023, with Envision moving up three positions to second place and Denmark’s Vestas in 3rd place. Windey and Mingyang occupy fourth and fifth place respectively, with the latter the world’s largest offshore wind turbine supplier in 2023. Sany and Dongfang round out the Chinese presence in the top 10. Still, 97 percent of Chinese company installations in 2023 were in their home market of China, the same level as the previous year. Chinese companies installed 2.3 GW outside of their home-market last year, with 63% of that in the Asia region.

Download the full report from our Market Intelligence area

Vestas, Siemens Gamesa, Nordex Group, GE Vernova and Enercon, remain the top five turbine suppliers in Europe, in 2023. Globally, Vestas fell two positions from 2022 to 3rd place, although with wind turbines installed in 36 countries the Danish OEM remains the most geographically diverse.

In terms of total global cumulative wind turbine installations, Vestas, Siemens Gamesa and GE Vernova remain the world’s Top-3 wind turbine suppliers at the end of 2023.

Ben Backwell, CEO of GWEC, said: “The data in this report paints a picture of a global industry that has entered a period of accelerated growth. However, that growth is concentrated in mature markets like China, the US and Germany. For wind energy to play its full role in the push to achieve Net Zero, growth needs to speed up across the globe, particularly in emerging and developing economies.

“The wind industry can thrive globally if governments collaborate with industry to implement the energy transition through supportive, long term policymaking and multilateral cooperation. Despite a record year for wind energy installations, we need to make faster progress to achieve climate goals, and make sure market conditions support a healthy global manufacturing supply chain. The industry is ready to work with its partners across the world to create conditions for long-term market growth, and deliver the tripling of renewables agreed at COP28.”

The Data

A total of 23,833 wind turbines were installed worldwide in 2023, manufactured by 30 different companies – of which 19 are from the Asia-Pacific region, 8 from Europe, 2 from America and 1 from the Middle East. Growth was mainly driven by orders from manufacturers’ home markets, namely China, the US, and Europe.

Goldwind installed 16.7 GW of capacity last year, to become the number one turbine supplier last year, with Envision moving up three positions to second place. Vestas fell two positions to 3rd place from 2022, although with wind turbines installed in 36 countries the Danish OEM’s new wind installations in 2023 increased by one percent compared with 2022. Windey and Mingyang occupy fourth and fifth place respectively, with the latter the world’s largest offshore wind turbine supplier in 2023.

Top 10 wind turbine suppliers in 2023

Feng Zhao, Head of Strategy and Market Intelligence,GWEC, said: “More than 120 GW capacity of wind turbine was mechanically installed worldwide in 2023, of which two third was delivered by Chinese wind turbine suppliers.

“Although the fierce price competition in China has been driving Chinese turbine OEMS to pursue opportunities in the overseas markets since 2021, 97 per cent of their installations in 2023 are still in their home market.

“Vestas, Siemens Gamesa, Nordex Group, GE Vernova and Enercon remain the top five turbine suppliers in Europe, in 2023. Chinese OEMs only installed 194.1 MW of wind turbines in Europe last year, of which only 8.4 MW was in the EU27.”

“Of the top 3 western OEMs, Vestas and Siemens Gamesa reported 155 MW and 3 MW installations in China in 2023, respectively, together accounting for only 0.2 per cent of the new installations in the world’s largest wind market.”

A note on the data:

The Global Wind Market Development – Supply Side Data 2023 represents a detailed account of wind turbines mechanically installed globally from all active suppliers over the past year – crucially this does not consider whether the turbines are grid-connected and commissioned.

The final report includes more than 30 tables and figures charting the evolution of global wind power markets on the supply side. This is the sister report to GWEC’s Global Wind Report 2024, which covers the global wind market status, based on annual grid-connected capacity.

Combining the two reports provides a powerful tool for our members to understand the global wind market development from both demand and supply sides.