For every nation, clean technology manufacturing can bring economic security, employment, and resilience to clean energy transitions, says the IEA. The sector is now so significant that it’s also impacting overall GDP performance: in 2023, clean technology manufacturing alone accounted for around 4% of global GDP growth and nearly 10% of global investment growth. Here, the IEA summarises its first-of-its-kind “Energy Technology Perspectives Special Report”, an analysis at a global and regional level. It’s designed to help policy makers prepare their industrial strategies. It focuses on five key clean energy technologies – solar PV, wind, batteries, electrolysers and heat pumps. As far as net-zero targets are concerned, solar PV is well ahead, batteries are well on track, wind looks promising.

The analysis breaks things down by geography, with China, the U.S., Europe and India having the most impact. Competition will decide the relative fortunes of each region. The analysis notes that labour costs and government subsidies are not the only drivers: the size of the domestic market, the availability of skilled workers, infrastructure readiness, permitting processes and other regulations, synergies with existing industries are just some examples. Hence, policy interventions can raise the attractiveness of investing in a given technology and reaping the benefits. The IEA ends with its recommendations to policy-makers.

Clean technologies shine a spotlight on manufacturing

The manufacturing sector – long an engine of economic growth and development – is increasingly at the forefront of considerations on energy, climate and economic policy. Countries are racing to capitalise on benefits that clean technology manufacturing can bring to economic security, employment and the resilience of clean energy transitions. Following a request by G7 Leaders in 2023, this Energy Technology Perspectives Special Report is designed to aid policy makers as they prepare their industrial strategies. It focuses on five key clean energy technologies – solar PV, wind, batteries, electrolysers and heat pumps.

Notes: CTM = Clean technology manufacturing. Shares of investment calculated as sectoral investment divided by gross fixed capital formation on a global basis. Sectors correspond to the following ISIC codes: ‘Pharmaceuticals’ = Division 21, ‘Basic chemicals’ = Group 201, ‘Steel’ = Groups 241-243, ‘Glass’ = Group 231, ‘Aerospace’ = Group 303.

Investment in clean technology manufacturing is becoming so significant that it is starting to register in broader macroeconomic data. In 2023, it accounted for around 0.7% of global investment across all sectors of the economy, driving more spending than established industries like steel (0.5%). In growth terms, the contribution is even starker – in 2023, clean technology manufacturing alone accounted for around 4% of global GDP growth and nearly 10% of global investment growth.

The recent surge in investment looks set to continue

New, first-of-its-kind analysis in this report shows that investment in clean technology manufacturing stood at around USD 200 billion in 2023, growing by more than 70% relative to 2022. Investments in solar PV and battery manufacturing plants led the way, together accounting for more than 90% of the total in both years. Investment in solar PV manufacturing more than doubled to around USD 80 billion in 2023, while investment in battery manufacturing grew by around 60% to USD 110 billion.

Notes: RoW = Rest of world. Solar PV includes facilities producing polysilicon, wafers, cells and modules; Batteries includes facilities producing packs and cells, anodes and cathodes; Wind includes facilities producing nacelles, blades and towers; Other includes electrolysers and heat pump manufacturing.

China accounted for three-quarters of global investments in clean technology manufacturing in 2023, down from 85% in 2022, as investment in the United States and Europe grew strongly – particularly for battery manufacturing, for which investments more than tripled in these regions. For solar PV manufacturing, investments in China more than doubled between 2022 and 2023. Outside these three major manufacturing hubs, India, Japan, Korea and countries in Southeast Asia made important contributions in specific areas, while investment in regions such as Africa, Central America and South America was negligible.

Near-term momentum for clean manufacturing looks strong. Around 40% of investments in 2023 were in facilities that are due to come online in 2024; for battery manufacturing facilities, this share is nearly 70%. Committed projects – those that are under construction or have reached final investment decisions – through 2025, together with existing capacity, would exceed by 50% the global solar PV deployment needs in 2030 based on the IEA’s Net Zero Emissions by 2050 Scenario (NZE Scenario) and meet 55% of battery cell requirements. This momentum is also spreading to adjacent sectors – nearly half of committed battery manufacturing announcements in the United States will be via joint ventures with automakers.

The project pipeline is expanding rapidly, if unevenly

Existing manufacturing capacity for solar PV modules and cells could today achieve what is necessary to meet demand under the NZE Scenario in 2030 – six years ahead of schedule, with only modest gaps remaining for the upstream steps of wafer and polysilicon manufacturing. However, facilities making cells and modules are currently seeing relatively low average utilisation rates of around 50% globally. Key factors that explain this are a solar PV module supply glut, together with the rapid expansion of manufacturing capacity. While the sharp increase in supply has driven down module prices, supporting wider consumer uptake, stockpiles of solar PV modules are growing and there are signs of downscaling and postponements of planned capacity expansions, particularly in China.

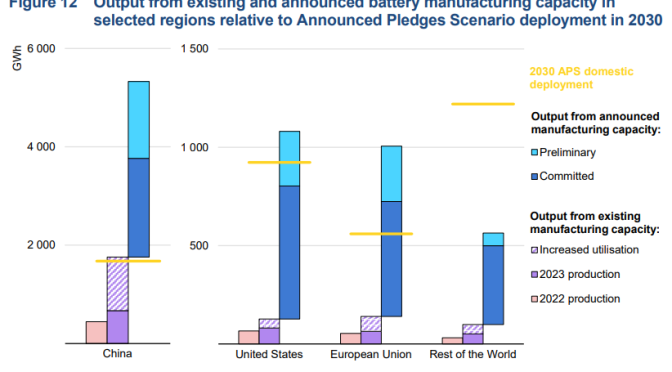

Battery manufacturing also had a record year in 2023. Production totalled more than 800 gigawatt-hours (GWh), rising 45% from 2022. Capacity additions also surged, with almost 780 GWh of cell manufacturing capacity added – around a quarter more than in 2022. This raised total installed capacity to around 2.5 terawatt-hours (TWh), or almost three times current demand. Globally, battery manufacturing capacity could exceed 9 TWh by 2030 if all announcements are realised. Battery manufacturing deployment needs in 2030 under the NZE Scenario are within reach: more than 90% could be met by announced expansions that have reached final investment decisions.

New manufacturing capacity for wind and electrolysers also grew faster in 2023, although the gains were not as dramatic. Existing capacity for wind could deliver nearly 50% of NZE Scenario needs in 2030, while announced projects could meet a further 12%. Meanwhile, capacity additions for heat pump manufacturing slowed due to stagnation in the majority of leading markets. Existing capacity could deliver only around one-third of 2030 needs in the NZE Scenario – though this could change quickly given the short lead times typical of capacity expansions in this industry.

Notes: 2030 value includes all operational capacity in 2023 together with the capacity of announced manufacturing projects through to 2030. For electrolysers, the analysis only includes projects for which location data was available. Shares are based on manufacturing capacity. Refer to the Technical annex for more details on the analytical boundaries and methodologies used in this analysis.

Geographic concentration in manufacturing looks set to remain high for most clean energy technologies

Notes: APS = Announced Pledges Scenario. 2023 production values reflect estimates of actual utilisation rates. Increased utilisation refers to the gap between 2023 production levels and existing capacity being utilised at 85%. A utilisation rate of 85% is used for both existing and announced manufacturing capacity in 2030. Refer to the Technical annex for more details on the analytical boundaries and methodologies used in this analysis.

China, the United States and the European Union together account for around 80% to 90% of manufacturing capacity for solar PV, wind, battery, electrolyser and heat pump manufacturing. Little change to this overall concentration is foreseen to 2030, even if all announced projects come to fruition.

Notes: APS = Announced Pledges Scenario. 2023 production values reflect estimates of actual utilisation rates. Increased utilisation refers to the gap between 2023 production levels and existing capacity being utilised at 85%. A utilisation rate of 85% is used for both existing and announced manufacturing capacity in 2030. Demand refers to both EV battery and stationary storage demand. Battery capacity refers to battery cells. Battery refers to lithium-ion batteries. Refer to the Technical annex for more details on the analytical boundaries and methodologies used in this analysis.

For battery cell manufacturing, the situation is somewhat different: planned capacity additions in Europe and the United States look set to reduce China’s present share of global capacity, with both regions reaching around a 15% share by 2030 if all announced projects are realised. In Europe and the United States, announced battery cell manufacturing capacity is sufficient to meet the 2030 domestic deployment needs associated with their own climate goals.

Notes: APS = Announced Pledges Scenario. The figure includes data on facilities which are specifically dedicated to wind manufacturing for blades, nacelles and towers, except for tower manufacturing in China, where an implausible shortfall is assumed to be met by additional generic fabrication capacity. 2023 production values reflect estimates of actual utilisation rates. A utilisation rate of 85% is used for both existing and announced dedicated manufacturing capacity in 2030. Refer to the Technical annex for more details on the analytical boundaries and methodologies used in this analysis.

The geographic concentration of manufacturing for wind, electrolysers and heat pumps also shows little change through 2030. Outside of the main producer countries, Central and South America account for a small share of global production of the main wind turbine components (4% to 6% for nacelles, blades and towers). However, virtually no clean technology manufacturing takes place in Africa today. Concentration is even more pronounced for upstream solar PV and battery components, but the prospect of surplus capacity may open up possibilities for greater diversification of production in this area.

Production cost gaps are significant, but not immutable

New data and analysis, including plant-level assessments of more than 750 facilities, provide insight into key drivers of manufacturing costs and the differences between regions. Our analysis shows that China is the lowest-cost producer for all the technologies highlighted in this report, before accounting for explicit supportive policy measures, though it also points to opportunities for reducing cost gaps.

The main upfront cost that contributes to overall production costs is the capital expenditure to set up a clean energy manufacturing plant, and the associated financing costs. Facilities in the United States and Europe are typically 70% to 130% more expensive per unit of output capacity than those in China for solar PV, wind and battery manufacturing, before accounting for the difference in the cost of capital between regions. India’s capital costs are around 20% to 30% higher than China’s, but significantly lower than those of the United States and Europe.

However, upfront costs make only a modest contribution to the overall levelised cost of manufacturing. Annualised capital expenditure amounts to just 15% to 25% of the total cost of producing solar PV modules, with a cost of capital of 8%. The proportions are similar for batteries (10-20%), wind turbines and heat pumps (2-10%) and somewhat higher for alkaline electrolyser stacks (15-30%). Operational costs, including energy, material, component and labour costs, make a far more important contribution in aggregate. Using global average commodity prices, and regional labour and end-user prices for energy inputs, ongoing operational costs account for 70% to 98% of total manufacturing costs. Reducing the costs of energy, materials and components is therefore an important lever for reducing cost gaps.

Cost is not the only factor that influences investment

Many factors besides the cost of manufacturing shape the decisions of firms to invest: the size of the domestic market, the availability of workers with the necessary skills, infrastructure readiness, permitting processes and other regulatory regimes, proximity to customers and synergies with existing industries are just some examples. Policy interventions can therefore raise the attractiveness of investing in a given region without directly subsidising the costs of manufacturing. Training and certification schemes for workers, compressing project lead times while maintaining environmental standards, enlarging domestic markets and reducing uncertainty with robust, stable climate policies are some key “low regret” measures that can increase incentives to invest, irrespective of the role of direct incentives in industrial strategies.

Innovation is another key focus for industrial strategy design; as the portfolio of energy technologies shifts towards mass-manufactured equipment, the energy sector is likely to include more R&D-intensive companies with factories and R&D hubs in their home countries and elsewhere in the world. Being at the frontier of innovation is an important opportunity to compete in the market, which is one reason why countries with relatively high labour and energy costs continue to manufacture goods in trade-exposed sectors. While private-sector R&D can be stimulated by policies that promote manufacturing investment and experience, direct innovation support is also needed. Government measures, including R&D grants or loans, project finance, support for rapid prototyping, start-ups and production scale-up, can be targeted towards specific innovation missions to advance manufacturing.

Key principles to support industrial strategy design

The purpose of this report is not to prescribe a single approach to industrial strategy or to make recommendations to a specific country, but rather to support decision-making. Alongside its analysis of competitiveness, innovation and other specific areas of policy, the report distils a set of key principles to guide policy makers.

When considering domestic actions, governments should:

- Prioritise and play to strengths, with clearly defined goals and metrics to gauge success, and with experimentation and the ability to change course built in.

- Attract and support innovators, including by creating strong links between manufacturing and each component of the broader innovation system.

- Plug cost gaps strategically and for the long-term, including through measures to reduce lead times and upskill workforces.

Governments should also collaborate internationally, which in turn enhances opportunities for domestic investment and global progress. To do so, they should:

- Collect data and track progress, including on the trade and production of clean technologies and their components.

- Co-ordinate efforts across supply chains to enhance resilience by sharing experiences and collaborating.

- Identify and build strategic partnerships, backed by clear frameworks for co-operation.