In the last week of May, prices in most European electricity markets fell compared to the previous week. Most markets registered negative prices at the end of the week. The increase in renewable energy production and the decrease in demand in some markets favored the decreases. On May 27, Portugal broke the all?time record for photovoltaic energy production with 21 GWh generated using this technology. Wind energy production increased in most markets.

Solar photovoltaic, solar thermoelectric and wind energy production

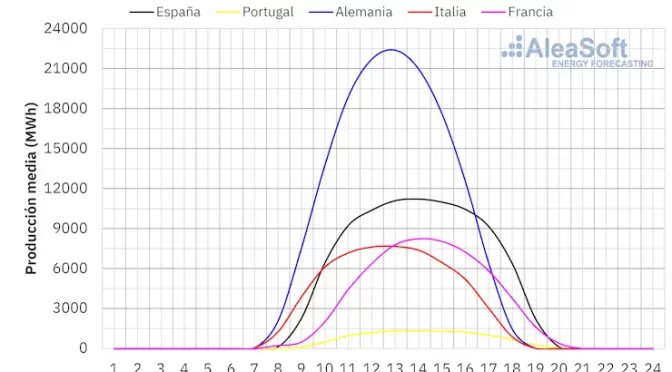

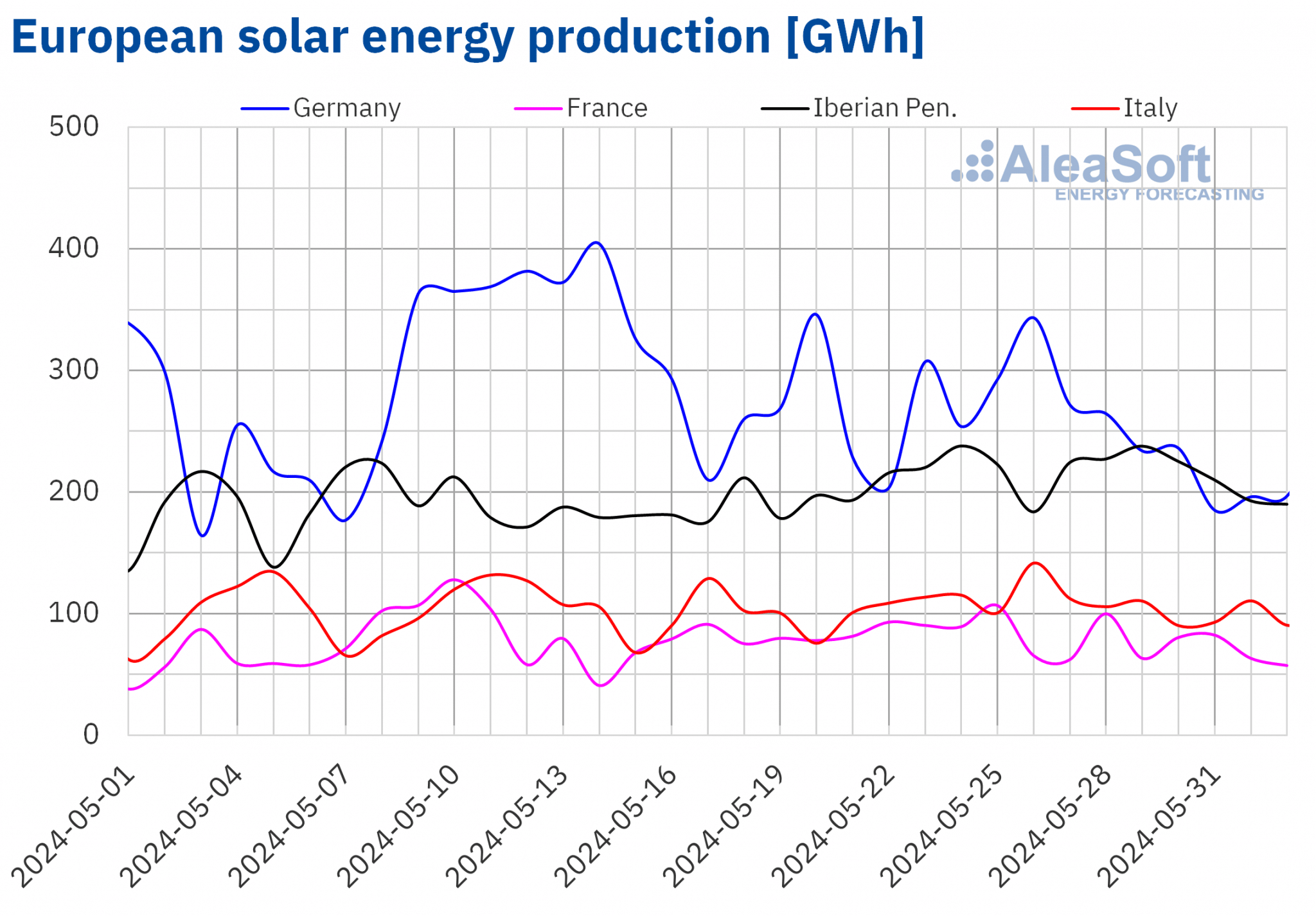

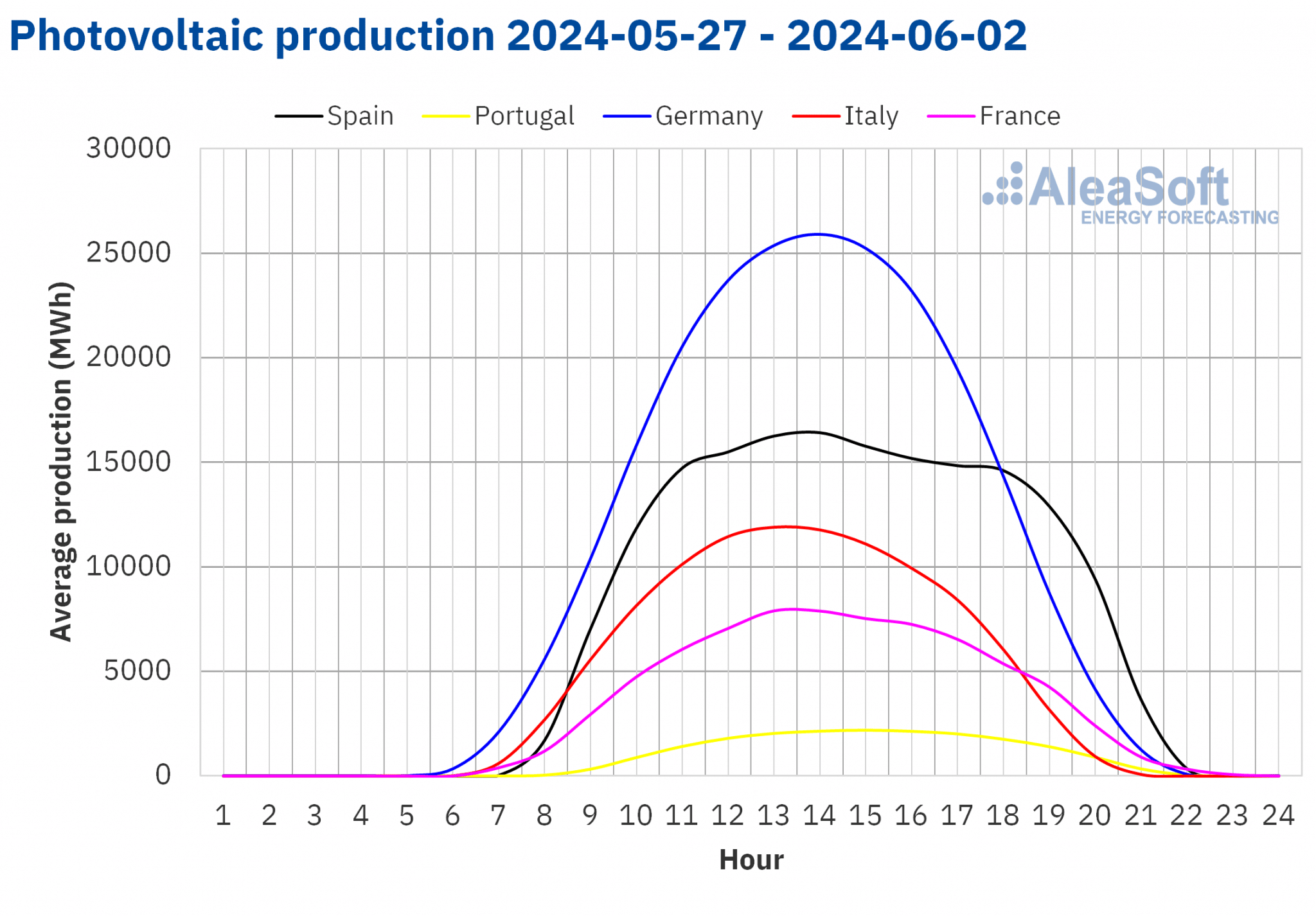

In the week of May 27, solar energy production decreased in most major European electricity markets compared to the previous week. Continuing the downward trend of the previous week, the German market registered the largest drop, 20%, while the Italian market registered the smallest drop, 5.8%. The exception was the Iberian Peninsula, where solar energy production increased for the second consecutive week, this time by 2.5%.

In addition, with a 9.8% week?on?week increase, the Portuguese market broke the historical record for daily solar photovoltaic energy production, 21 GWh, on May 27.

In the week of June 3, according to AleaSoft Energy Forecasting’s solar energy production forecasts, it will decrease in Spain and Italy, while it will increase in Germany.

Source: Prepared by AleaSoft Energy Forecasting using data from ENTSO-E, RTE, REN, Red Eléctrica and TERNA.

Source: Prepared by AleaSoft Energy Forecasting using data from ENTSO-E, RTE, REN, Red Eléctrica and TERNA.

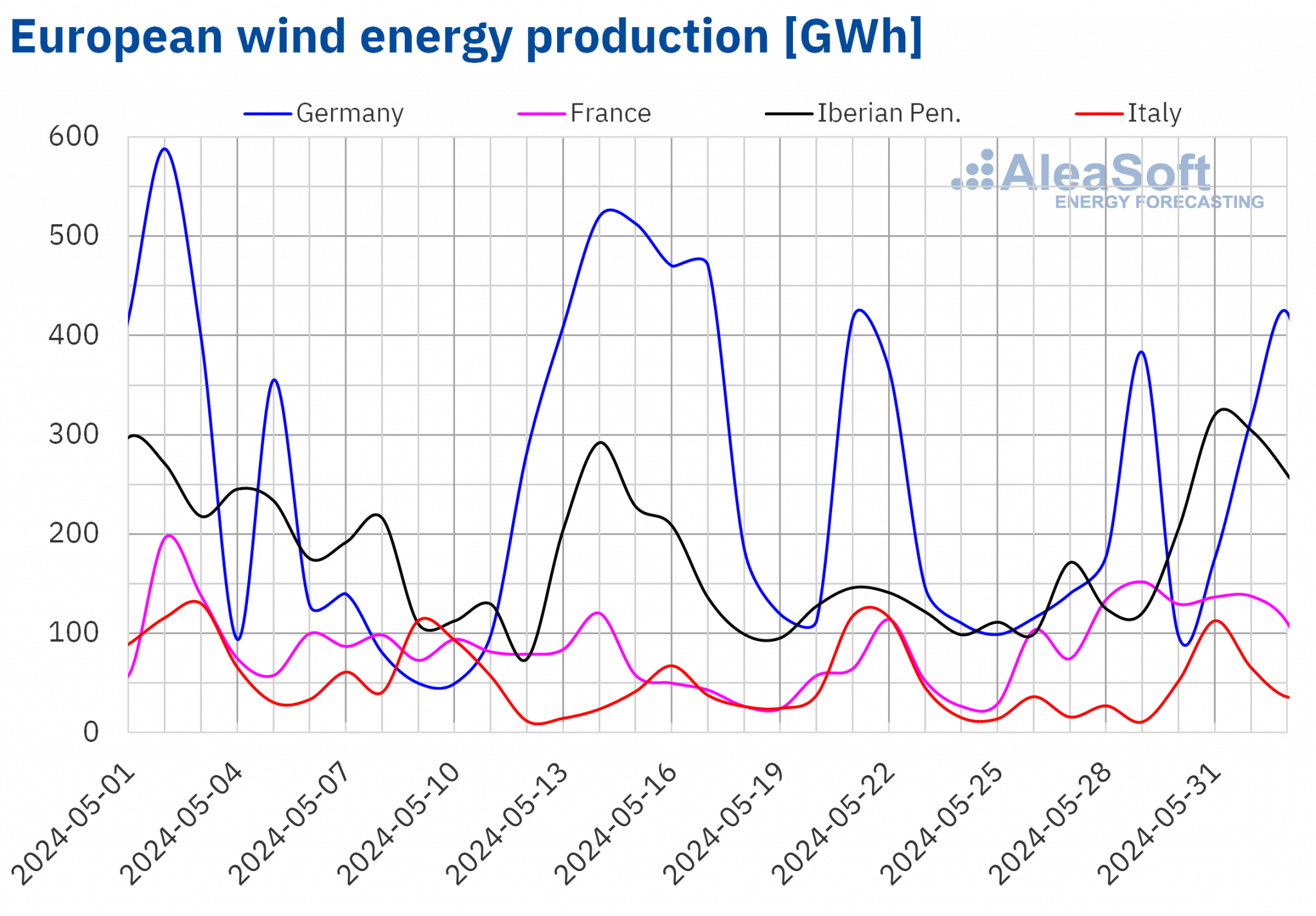

In the week of May 27, wind energy production increased in most major European electricity markets compared to the previous week. The French market continued the upward trend of the previous week and registered the largest increase, 96%. The rest of the markets reversed the previous week’s decline and registered increases between 25% and 80%. Only the Italian market registered a drop in wind energy production, which was 16%.

In the week of June 3, according to AleaSoft Energy Forecasting’s wind energy production forecasts, production using this technology will decrease compared to the previous week in all analyzed markets.

Source: Prepared by AleaSoft Energy Forecasting using data from ENTSO-E, RTE, REN, Red Eléctrica and TERNA.

Electricity demand

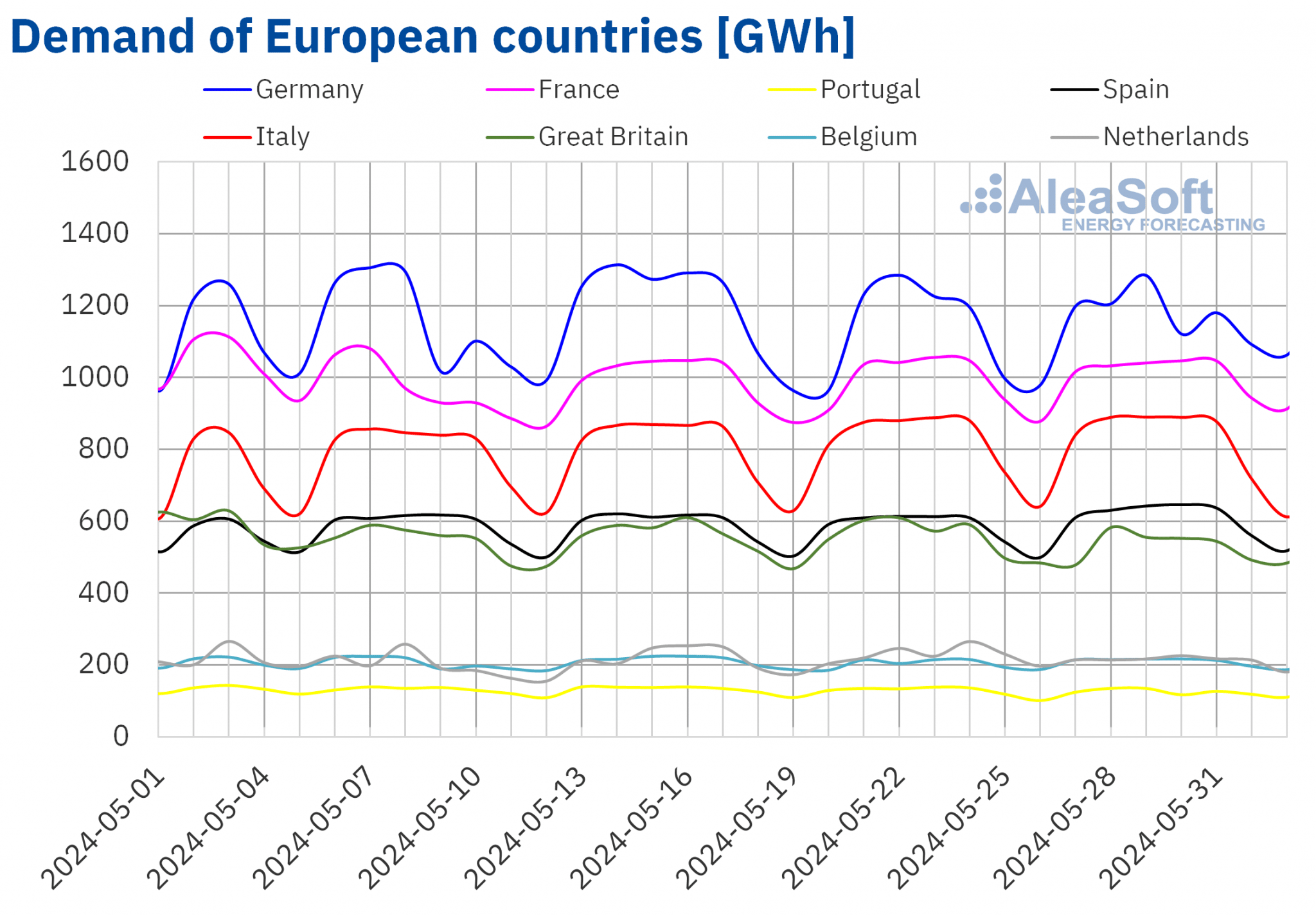

During the week of May 27, the inter-week variations in electricity demand in the main European electricity markets were heterogeneous. Demand increased in the German, French, Spanish and Belgian markets, reversing the downward trend of the previous week. Within this group, the Spanish market registered the largest increase, 4.0%, and the French market the smallest increase, 1.9%. In Italy, demand was similar to that of the previous week. On the other hand, in the Netherlands, Great Britain and Portugal, demand decreased from 6.5% to 2.8%. The drop in demand was related to the Spring holiday in Great Britain on Monday, May 27, and the Corpus Christi celebration in Portugal on Thursday, May 30.

During the last week of May, average temperatures increased in some markets. Increases ranged from 0.3 °C in Great Britain to 3.2 °C in Portugal. In contrast, average temperatures decreased from 0.4 °C in Germany to 1.0 °C in the Netherlands.

For the week of June 3, according to AleaSoft Energy Forecasting’s demand forecasts, demand will increase in Italy, Portugal, the Netherlands, France, Spain and Great Britain. Demand will only decrease in Belgium, while it will remain at the same level as the previous week in Germany.

Source: Prepared by AleaSoft Energy Forecasting using data from ENTSO-E, RTE, REN, Red Eléctrica, TERNA, National Grid and ELIA.

European electricity markets

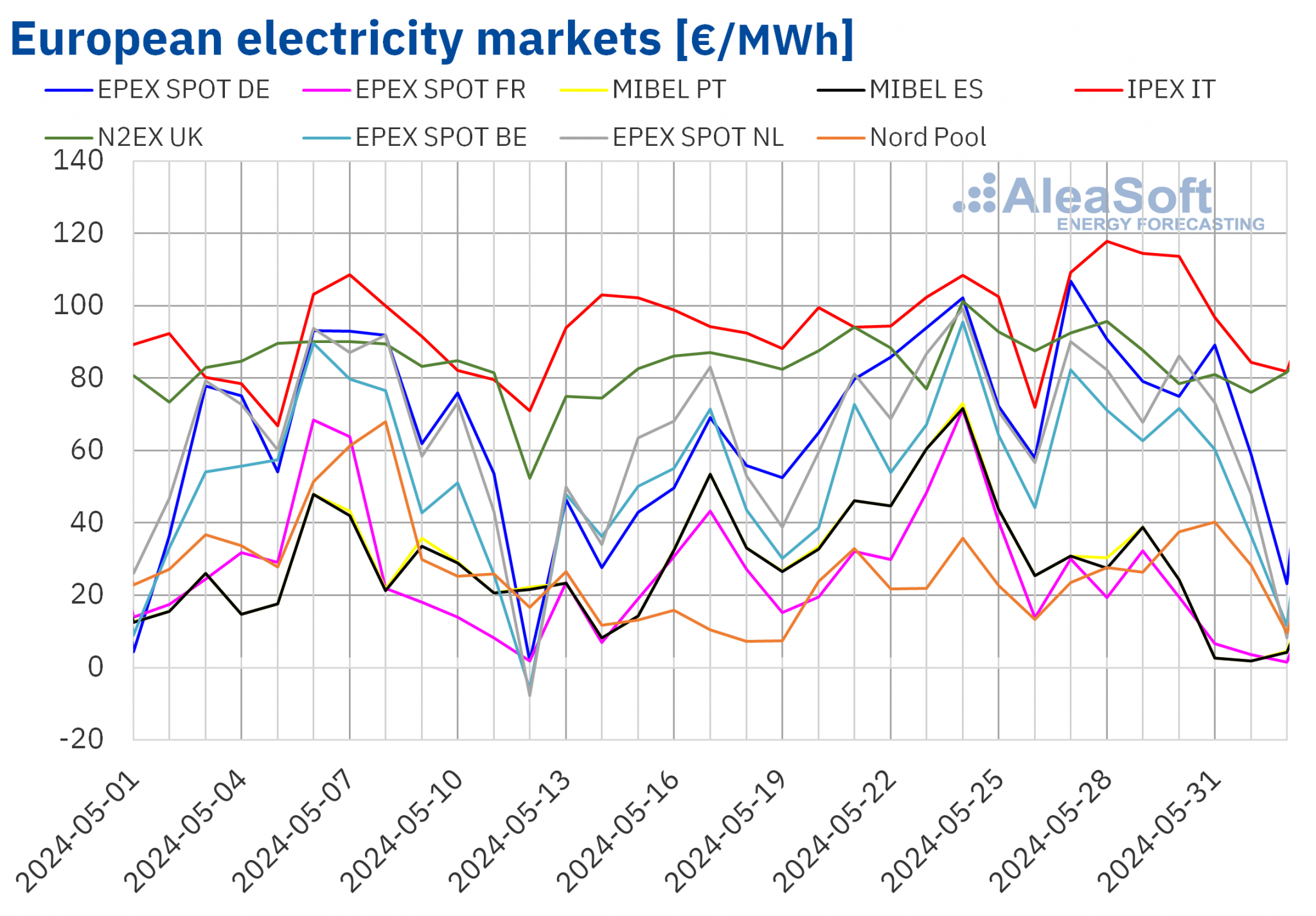

In the last week of May, prices in most major European electricity markets fell compared to the previous week. The exceptions were the IPEX market of Italy and the Nord Pool market of the Nordic countries, with increases of 6.7% and 12%, respectively. On the other hand, the EPEX SPOT market of France and the MIBEL market of Portugal and Spain had the largest percentage price drops, 56%, 59% and 60%, in each case. In the other markets analyzed at AleaSoft Energy Forecasting, prices fell between 5.6% in the N2EX market of the United Kingdom and 13% in the EPEX SPOT market of the Netherlands.

In the last week of May, weekly averages exceeded €55/MWh in most analyzed European electricity markets. The exceptions were the French, Spanish, Portuguese and Nordic markets, with averages of €16.13/MWh, €18.61/MWh, €19.08/MWh and €27.60/MWh, respectively. On the other hand, the Italian market registered the highest weekly average, €102.60/MWh. In the rest of the analyzed markets, prices ranged from €56.58/MWh in the Belgian market to €84.71/MWh in the British market.

Regarding hourly prices, most analyzed European markets registered negative prices on Sunday, June 2. The exceptions were the British and Italian markets, which did not register negative prices in the last week of May. On the other hand, the Belgian and Dutch markets also registered negative prices on Saturday, June 1. In the case of the Spanish, French and Portuguese markets, in addition to the weekend, these markets also registered negative prices on Friday, May 31. The Dutch market registered the lowest hourly price of the last week of May, ?€81.00/MWh. This price corresponded to Sunday, June 2, from 15:00 to 16:00.

During the week of May 27, increased wind energy production and lower demand in some markets exerted their downward influence on European electricity market prices. The increase in solar energy production in the Iberian Peninsula also contributed to lower prices in the MIBEL market. In contrast, production with these technologies decreased in Italy. This, together with a slight increase in the average gas price, led to higher prices in the IPEX market.

AleaSoft Energy Forecasting’s price forecasts indicate that they will increase in most analyzed European electricity markets in the first week of June, influenced by a decrease in wind energy production and an increase in demand in most cases. In addition, in markets such as Spain and Italy, solar energy production will fall, favoring the expected price increase.

Source: Prepared by AleaSoft Energy Forecasting using data from OMIE, EPEX SPOT, Nord Pool and GME.

Brent, fuels and CO2

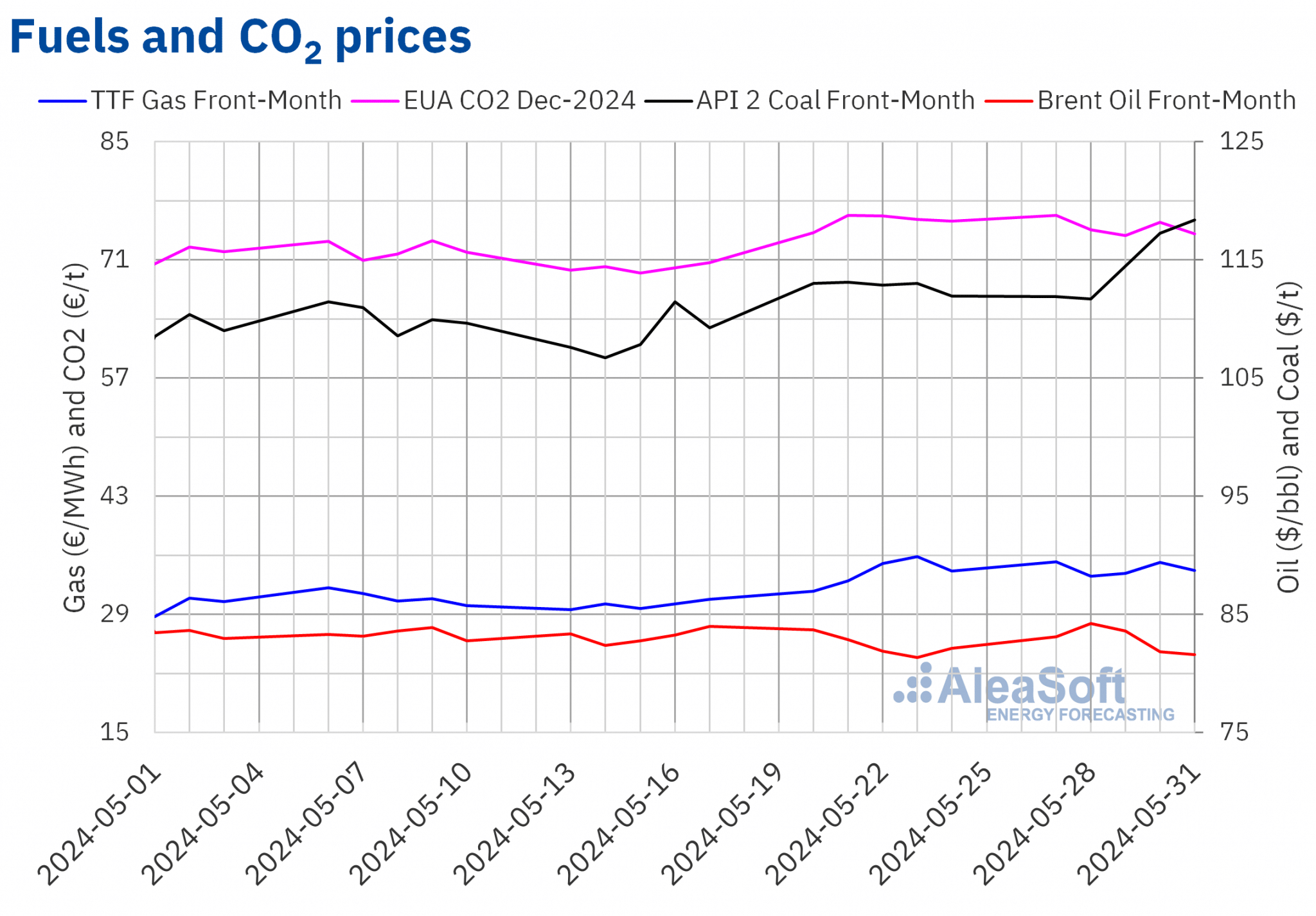

Brent oil futures prices for the Front?Month in the ICE market increased in the first sessions of the last week of May. They reached their weekly maximum settlement price, $84.22/bbl, on Tuesday, May 28. This price was the highest in the month of May. However, prices declined during the rest of the week. As a result, on Friday, May 31, these futures registered their weekly minimum settlement price, $81.62/bbl. According to data analyzed at AleaSoft Energy Forecasting, this price was 0.6% lower than the previous Friday. The average settlement price for the week was 0.6% higher than the previous week’s price.

At the beginning of the last week of May, news of the increase in Goldman Sachs’ 2030 oil demand forecasts exerted its upward influence on Brent oil futures prices. However, concerns about demand continued and contributed to the decline in prices in the last sessions of the week. Inflation data from the United States also favored the decline in prices. On the other hand, on Sunday, June 2, OPEC+ agreed to maintain its production cuts until the end of 2025.

As for TTF gas futures prices in the ICE market for the Front?Month, in the last week of May they remained stable, oscillating around €34/MWh ? €35/MWh. On Monday, May 27, these futures reached their weekly maximum settlement price, €35.24/MWh. According to the data analyzed at AleaSoft Energy Forecasting, this price was the second highest settlement price since the end of December 2023. However, after a decrease of 4.8%, on Tuesday, May 28, they registered their weekly minimum settlement price, €33.53/MWh. In the last session of the week, on Friday, May 31, the settlement price was €34.22/MWh, 0.3% higher than the previous Friday. For the week as a whole, the average settlement price was 1.4% higher than the previous week.

In the last week of May, forecasts of high temperatures in Europe exerted an upward influence on TTF gas futures prices. High temperatures would also affect Asia, which contributed to increased demand for liquefied natural gas in Asian markets. However, high European reserve levels and gas supplies from Norway contributed to keeping prices below €36/MWh.

Regarding settlement prices of CO2 emission allowance futures in the EEX market for the reference contract of December 2024, in the last week of May they continued above €70/t. On Monday, May 27, these futures reached their weekly maximum settlement price, €76.25/t. Instead, on Wednesday, May 29, these futures registered their weekly minimum settlement price, €73.86/t. At the end of the week, on Friday, May 31, the settlement price was €74.10/t. According to the data analyzed at AleaSoft Energy Forecasting, this price was 2.0% lower than the previous Friday. In the last week of May, the average settlement price was 1.0% lower than the previous week.

Source: Prepared by AleaSoft Energy Forecasting using data from ICE and EEX.

AleaSoft Energy Forecasting’s analysis on the prospects for energy markets in Europe and the renewable energy projects financing

The 45th webinar of the monthly webinar series of AleaSoft Energy Forecasting and AleaGreen will take place on Thursday, June 13. The topics to be covered in this webinar are the evolution of European energy markets and the prospects in the second half of 2024, the growth opportunities in the renewable sector, the regulatory and design challenges of the wholesale market and the current affairs of the PPA market in Spain. The June webinar will feature guest speakers from Engie Spain for the sixth time.