Exploring Europe’s energy storage gigawatt-scale revolution, and the hydrogen roadmap to 2030 and beyond.

The decarbonisation of Europe’s energy offers vast opportunities, yet also comes with significant challenges, particularly around renewable power and the integration of new wind and solar supply in systems. As renewables are rolled out, system flexibility and electricity demand have struggled to keep pace with the rapid growth in variable supply.

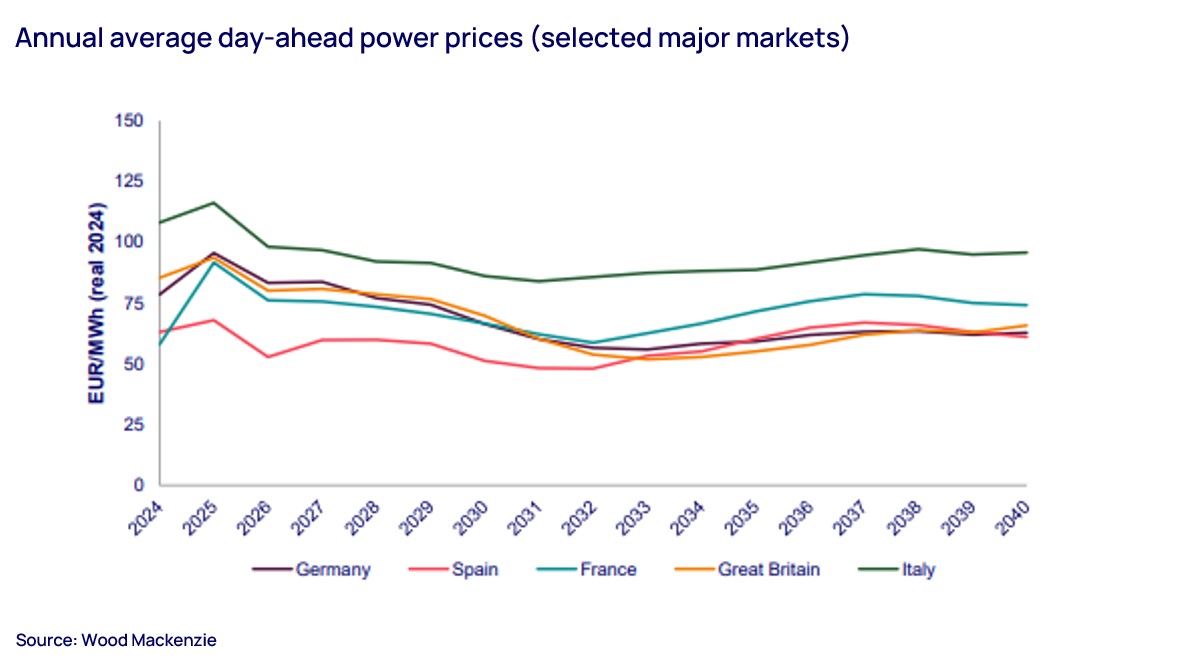

To learn more, download an extract from last week’s European power and renewables briefing in London by filling out the form at the top of this page, or read on for a summary of some of the key takeaways.

The opportunities and challenges facing European power

Over 50% of Europe’s power is now supplied from renewable resources. But as dispatchable fossil-fuelled power plants are retired, maintaining security of supply in the region’s rapidly evolving markets, and limiting the curtailment of renewables, is a growing challenge.

The sustained commitment of Europe’s policymakers to delivery of rapid decarbonisation, with the power sector at the forefront of that change, has resulted in a marked divergence in the pace of transitions in supply, demand and flexibility – developing new supply is comparatively easy, delivering the resulting energy to consumers when it is needed, and at the right cost is becoming more difficult.

Energy storage will play a vital role in providing the flexibility necessary to accommodate the changing characteristics of power production. Europe’s battery fleet will grow strongly in the coming years but, despite this, the dominant role of variable resources will see power price volatility rise in all markets.

But while far reaching changes will be seen, some long established fundamentals continue to play a central role in power price formation, particularly at the level of annual wholesale prices. Through the 2020s, gas will continue to exert a major influence on power prices, with the arrival of new LNG into the global gas market resulting in European power prices falling towards 2030. As this change develops, power supply will continue to be decarbonised by new wind and solar, while electricity demand growth struggles to keep pace. Widescale electrification becomes increasingly vital to system balance in the 2030s, offering essential supporting to prices and the economics of continued decarbonisation.

{kind=link}

Europe’s energy storage gigawatt-scale revolution

A gigawatt revolution is set to reshape Europe’s energy landscape. Solar-plus-storage has become the cheapest stable and uninterrupted source of electricity and there is an abundance of resources available across the region. But as Europe surpasses 50% of its power supply from renewable sources, integration challenges are growing.

The need for flexible energy storage solutions is now essential to addressing these integration issues. Standalone storage will make up the majority of the new energy storage capacity, but from 2027 onwards, the use of hybrid and co-located storage systems will grow significantly.

Fourteen European governments are finally recognising the role of storage and are including it in their national energy plans. Importantly, they are also releasing funding to support the rollouts.

The hottest European energy storage markets are currently in the spotlight and storage developers are trying to expand their businesses. What makes a market a hot market is dependent on three factors: regulation, depth of the market and market fundamentals such as interconnection or share of renewables. Considering that Europe hottest market are:

- The UK and Germany lead across all drivers.

- Poland and Italy are strong on regulation and bankability thanks to CM and MACSE.

- Benelux has strong fundamentals but is behind Germany.

- The Nordics are opening up to batteries, with CM coming to the picture and high ancillary service prices.

In the long term, fair market regulation and policy support will drive investments in energy storage projects. Final project revenue will depend on full revenue stack, but capacity mechanisms (CM) and power purchase agreements (PPA) will provide the minimum contracted revenue threshold across the region.

Hydrogen: mapping the road to 2030 and beyond

With the majors intensifying their decarbonisation targets with hydrogen expansion, exciting opportunities are opening up for investors who can capitalise on the growing demand for clean hydrogen solutions and the building of critical infrastructure.

The push towards FID for many hydrogen projects is being driven by a combination of factors. Captive demand, the targeting of the export markets and decarbonisation targets are pushing both players and governments to act.

Major energy companies and gas giants are leading the post-FID hydrogen drive and are using their expertise and infrastructure to decarbonise their existing facilities. While their dominance is set to continue, a total of US$38 billion has been invested in post-FID low-carbon hydrogen projects. This is targeting 6 million tonnes of production per annum (Mtpa).

Public subsidies are playing a crucial role in bridging the investment gap by providing the necessary financial support to move projects forward. This has led to a wave of projects that are now transitioning from planning stages to development through to 2030. A total of US$50 billion in public funding and subsidies has been allocated to support 5.65 Mtpa of capacity that has not yet reached FID.

Enabling adoption of hydrogen renewables is supported by funding schemes, demand incentives, strong policies across the value chain, close proximity to demand and low-cost raw materials.

By 2030, the low-carbon hydrogen market is expected to reach a capacity of 14 Mtpa but will need an investment of US$1.2 trillion. Reaching this target will require an accelerated pace of investment from 2024 onwards increasing by 1.3 times on average year-over-year to meet the projected capacity. The main obstacles to this happening are high costs, regulatory uncertainty, a reduction in demand, strict emissions requirements and insufficient midstream infrastructure.

What to look for in 2025

Our analysts have looked at how the renewable landscape will change in 2025 and anticipate hybrid systems and co-location storage emerging with solar hitting a record 25 MWdc. Onshore wind will face challenges but 14GW will be auctioned and offshore tender activity will rise by 30%. High gas costs will keep power prices high but decarbonisation goals are strong and renewables will be the majority energy supply.